ETFs

ProShares UltraPro QQQ ETF: Beware of Tail Risks (NASDAQ: TQQQ)

index charts including the NASDAQ Composite

travelpixpro

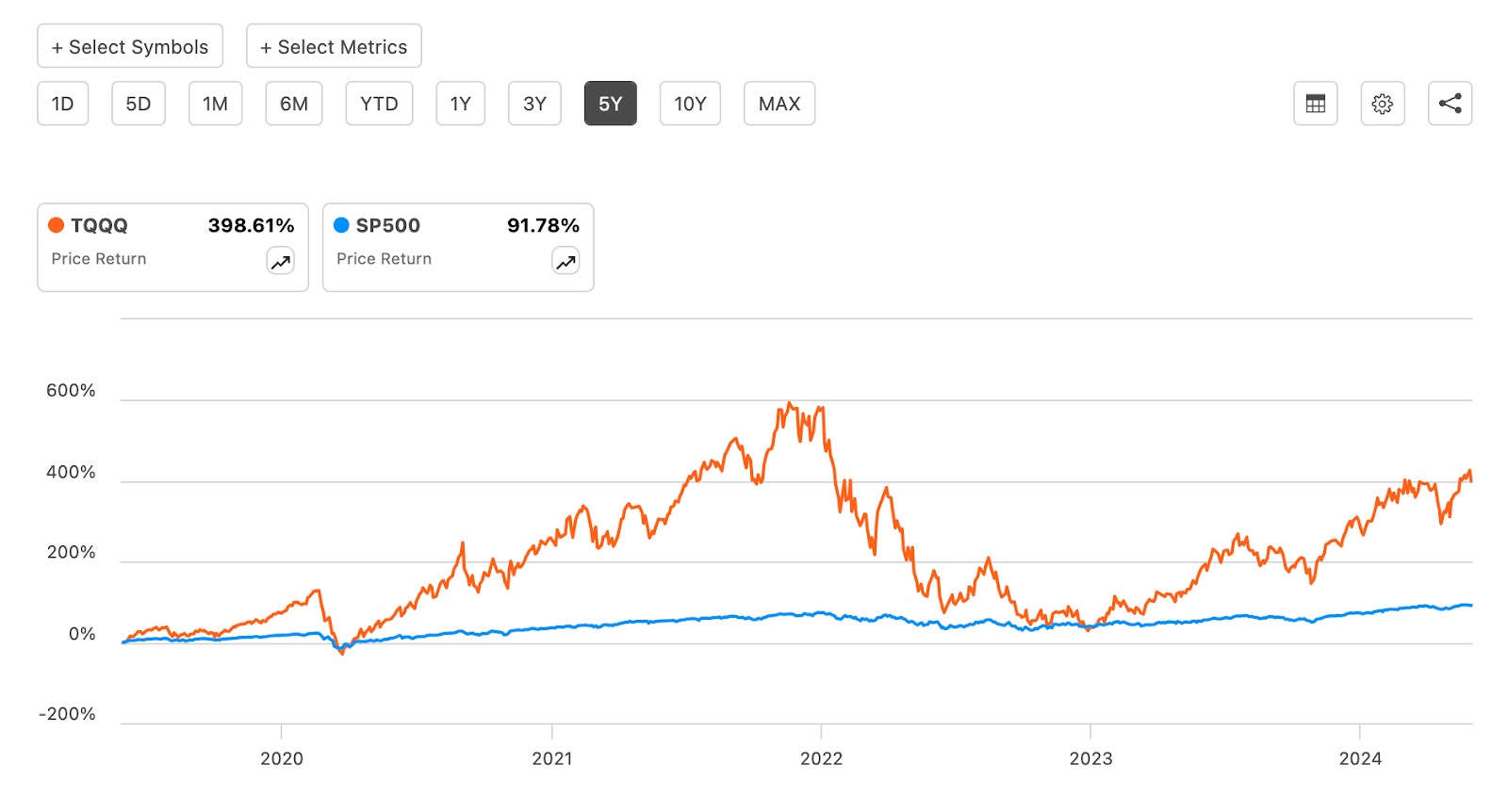

ProShares UltraPro QQQ ETF (NASDAQ:TQQQ) is one of the most popular leveraged ETFs on the market. By giving you three times the daily net asset value return of the NASDAQ-100 Index (before fees), it has the potential to perform very well in tech bull markets. However, when looking at the price history of TQQQ, we immediately notice something peculiar: the fund is off compared to its 2021 highs, even though the NASDAQ-100 has set new highs this year.

TQQQ vs QQQ Chart (Looking for Alpha Quant)

How is it that the TQQQ has been declining since 2021, while the NASDAQ-100 is increasing in the same period? It appears that UltraPro QQQ’s performance was lower than the index’s performance, rather than three times the index’s performance.

Well, if you look at the fund fact sheet, you will immediately see part of the problem: the costs. UltraPro QQQ charges a net fee of 0.88%, which isn’t exorbitant, but high enough to have a measurable impact on returns. These include more than four times the fees charged by Invesco’s unleveraged companies. Trust QQQ (QQQ) ETF Fees. This will have an effect on returns, you can be sure of that.

The real issue, however, is how exactly UltraPro QQQ delivers its “three times QQQ before fees” return. For an asset to deliver a multiple of another asset consistently, it must use leverage. Borrowed money is the most common form of leverage. There are others. For example, options have implied leveragebecause their “multiple of asset return or nothing” risk/reward profile is similar to that of purchasing an asset with borrowed funds.

In TQQQ’s 2023 Annual Report, ProShares CEO Marc Sapir listed leverage – particularly the increasing cost of leverage – as a risk factor for its fund. Between early 2022 and mid-2023, interest rates rose from near zero to 5%. This means that the cost of borrowing and using TQQQ derivatives has increased. As a result, it now costs more than in 2021, up to 3 times the QQQ yield before fees and interest. The result was that TQQQ not only did not triple the return of QQQ, but its price fell at the same time that QQQ rose!

In a recent article, I wrote that the Invesco QQQ Trust was investable despite its spectacular growth over the course of a year. My reasoning was that QQQ was worth the high multiples it was trading at because its major components were growing rapidly. I always think this way. However, I don’t think current market conditions are appropriate for leveraged bets on big tech stocks, because there is some risk in the big tech stocks themselves, and leverage has become expensive over the past two years. For this reason, I take a dimmer view of TQQQ than QQQ itself, as it risks underperforming after fees.

The costs of leverage

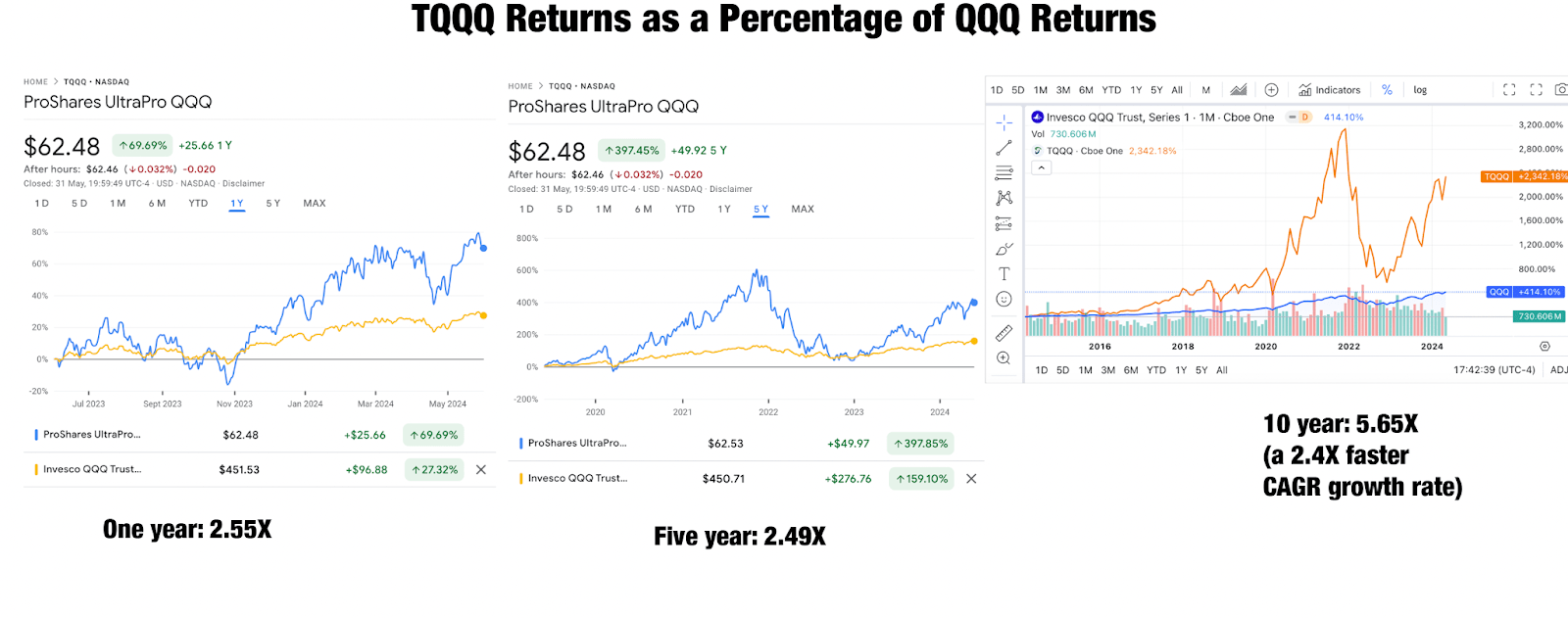

If you look at the TQQQ chart over a normal time frame, you will see that it does not actually triple the return of QQQ. Below I have compiled charts of QQQ and TQQQ over 12-month, five-year, and 10-year periods. As you can see, TQQQ’s returns ranged between 249% and 565% of those of QQQ. Over a 10-year period, performance was more more than three times that of QQQ, but this does not reflect a 3 times higher return on a compound annual basis (“CAGR”). On a CAGR basis, TQQQ grew 2.4 times faster than QQQ over 10 years, which is consistent with the one-year return shown below.

TQQQ vs QQQ Returns (Charts from Google Finance and Seeking Alpha Quant, author labels)

The question is: why is this happening? Although a 0.88% management fee represents a substantial cost, it cannot by itself explain why UltraPro QQQ only provides 5/6ths of the return it is expected to produce. This certainly doesn’t explain the fund’s decline from its 2021 highs, while QQQ itself is down. up 11.5% from these levels.

A big part of the problem is the cost of all that leverage. When interest rates rise, loans become more expensive and call option premiums increase. In June 2014, when the TQQQ increased by 2,000%, interest rates were close to 0%. They remained low through the end of 2021. This likely had a major influence on UltraPro QQQ’s 10-year performance. TQQQ’s underperformance relative to QQQ from November 2021 to today almost perfectly tracks the rise in interest rates from January 2022 to June 2023. ProShares executives even highlighted this fact in their 2023 annual report, in which interest rate increases were cited as a risk factor for UltraPro QQQ.

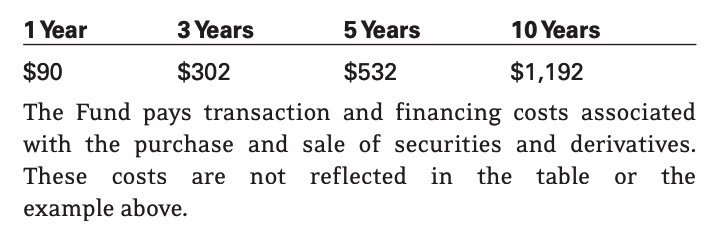

So what does UltraPro QQQ actually pay in option premiums and interest? This is not disclosed anywhere in the fund’s prospectus, although the document states that these costs are Do not be part of of the reported expense ratio of 0.88%.

TQQQ Costs (ProShares)

Although the total cost of TQQQ’s debt and derivatives is not publicly available, the parent company’s recent annual report contains some details on the costs of specific instruments purchased or borrowed by UltraPro QQQ. These included:

-

Rates average around 5.5% on swaps.

-

Quarterly exposure to derivatives at 240%.

-

435 long futures contracts with $120 million notional principal.

-

$39 billion notional principal on swaps – higher than fund assets under management!

The amount of these instruments and the rates paid on the swaps together indicate that the total expenses of UltraPro QQQ are well above the 0.88% announced. The company itself says so, and a 0.88% management fee alone would not explain TQQQ’s performance after 2021. It would seem likely that the true cost of running UltraPro QQQ is between 5% and 6%.

NAV calculated daily

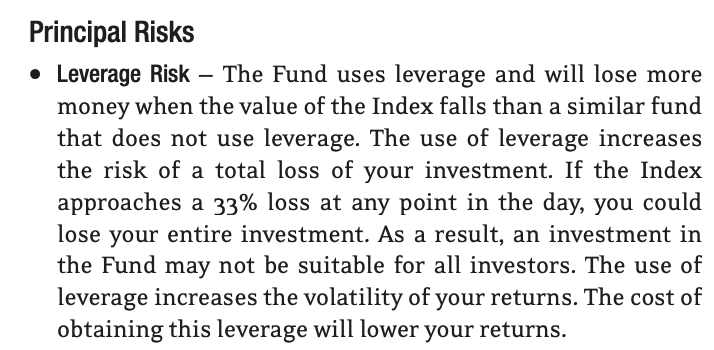

Another factor that may cause the TQQQ’s performance to differ from that of the Index is the daily calculation of the NAV. If the price of QQQ fell 33% in a single day, the fund’s net asset value would fall to near zero and investors would be wiped out. The fund’s prospectus clearly states this.

Now, the chances of the NASDAQ-100 falling in value by 33% in a single day are pretty low, but the logic above helps illustrate why the UltraPro QQQ sometimes deviates from the “3X” return it targets to offer. Mainly, the fact that the fund is designed to provide this tripling on a daily basis. This is not the same as a 3X return over an investor’s entire holding period. If the price of the NASDAQ-100 were to fall by 33.33% in a single day, then the TQQQ would likely go to zero and thus provide a return of -100%, which would in effect be three times the return of the NASDAQ-100 for this day. However, all of the fund’s assets would be wiped out and investors would not experience the subsequent rise in the index: three times zero equals zero. Smaller variations from this extreme scenario explain why TQQQ returns are not three times those of the index over all periods.

TQQQ Leverage Risk (ProShares)

Why I don’t recommend going long TQQQ at this time

UltraPro QQQ has been a great buy at times in the past. If you bought the fund when it was created in 2010 and held it until today, you would gain several thousand percentage points.

Knowing this, why do I advise against purchasing TQQQ today?

Mainly because the extreme magnitude of leverage and its increasing cost argue in favor of such a practice. At today’s prices, the NASDAQ-100 is trading at 32.9 times earnings, which is near the upper end of its 10-year range. If history is any indication, then the price of QQQ needs to fall to trade at its usual valuation.

Today, the current market situation is unique, with generative AI generating huge growths, especially for chipmakers like Nvidia (NVDA). This is why I rated QQQ a Buy in my last coverage. I knew the multiples were high when I wrote this article, but I still considered it a buy because I believed that just two years of growth at the rate we’ve seen lately would allow QQQ to catch up its valuation.

But even though I considered QQQ a Buy the last time I talked about it, I don’t think its leveraged cousin is a Buy today. For what? Well, as I explored in detail in this article, TQQQ has become more expensive to operate. Its past performance may therefore not be indicative of its future performance.

Specifically, I rated QQQ a “buy” rather than “strong buy” for a reason. I only had a small amount of belief in the call, and I didn’t really negotiate on it myself. I think there is a significant possibility that the price of Invesco QQQ Trust will decline over the next year. I think the chances of positive capital appreciation over the next year are higher, but not by much. Thus, an unleveraged position in QQQ with a modest portfolio weighting is justifiable for an investor with above-average risk tolerance and ability to bear risk.

But my conviction here is not high enough to justify a leveraged bet, and the many worst-case scenarios such bets expose investors to. My overall opinion on TQQQ is therefore neutral. It could really rebound in a best-case scenario, but TQQQ’s many risks outweigh the benefits of going long the fund with a heavy portfolio weighting as of today’s price.