ETFs

Leveraged ETF Dashboard and Lessons from the SPXL (NYSEARCA: SPXL) Story

Dilok Klaisataporn/iStock via Getty Images

ProShares Direxion Daily S&P 500 Bull 3x Shares ETF (NYSEARCA:SPXL) is one of the most popular instruments for trading in bullish market conditions. It is equivalent to ProShares UltraPro S&P 500 ETF 3x shares (UPRO). The 3X daily leverage factor is a source of drift, which can be positive or negative. It must be closely monitored to detect changes in drift regime. This article explains what “drift” means, quantifies it in 22 leveraged ETFs, and comments on historical data on SPXL.

Why do leveraged ETFs drift?

Leveraged ETFs often underperform their underlying index due to the same factor. ETF degradation can come from four factors: beta slippage, roll yield, tracking errors, and management costs. Beta slippage is the main factor in leveraged equity ETFs. To understand this, imagine a very volatile asset that rises 25% one day and falls 20% the next. A perfect 2x leveraged ETF rises 50% on the first day and falls 40% on the second day. At the close of the second day, the underlying asset returns to its initial price:

(1 + 0.25) x (1 – 0.2) = 1

At the same time, the perfectly leveraged ETF lost 10%:

(1 + 0.5) x (1 – 0.4) = 0.9

This is the normal effect of leverage and rebalancing. In a trending market, beta slippage can be positive. If the underlying index rises 10% two days in a row, on the second day it is up 21%:

(1 + 0.1) * (1 + 0.1) = 1.21

Perfect 2x leveraged ETFs are up 44%:

(1 + 0.2) * (1 + 0.2) = 1.44

Additionally, beta slippage is path dependent. If the underlying index gains 50% on day 1 and loses 33.33% on day 2, it returns to its initial value, as in the first example. However, the 2x ETF loses a third of its value, instead of 10% in the first case:

(1 + 1) x (1 – 0.6667) = 0.6667

Without demonstration, this shows that the higher the volatility, the greater the decay.

Monthly and annual drift monitoring list

There is no standard definition of leveraged ETF drift. Mine is based on the difference between the performance of the leveraged ETF and Ñ times the performance of the underlying index over a given time interval, if Ñ is the leverage factor. Most of the time, this factor sets a daily target against an underlying index. However, certain dividend-oriented leveraged products have been defined with a monthly objective (for most of the ETNs that have disappeared: CEFL, BDCL, SDYL, MLPQ, MORL, etc.).

First, let’s start by defining “yield”: it is the return of a leveraged ETF in a given time interval, including dividends. “IndexReturn” is the return of an unleveraged ETF on the same underlying asset in the same time interval, including dividends. “Abs” is the absolute value operator. The “drift” is calculated as follows:

Drift = (Return – (ReturnIndex x Ñ))/ Abs(Ñ)

“Decomposition” means negative drift.

|

Hint |

NOT |

Teleprinter |

Return 1 month |

One month drift |

One year return |

Drift over 1 year |

|

S&P500 |

1 |

5.40% |

0.00% |

28.04% |

0.00% |

|

|

2 |

10.34% |

-0.23% |

51.03% |

-2.53% |

||

|

-2 |

-9.09% |

0.86% |

-32.15% |

11.97% |

||

|

3 |

15.60% |

-0.20% |

77.34% |

-2.26% |

||

|

-3 |

-13.44% |

0.92% |

-46.42% |

12.57% |

||

|

ICE US20+ Bond T |

1 |

2.13% |

0.00% |

-8.85% |

0.00% |

|

|

3 |

4.99% |

-0.47% |

-38.80% |

-4.08% |

||

|

-3 |

-5.12% |

0.42% |

36.18% |

3.21% |

||

|

NASDAQ100 |

1 |

6.92% |

0.00% |

30.38% |

0.00% |

|

|

3 |

21.18% |

0.14% |

82.60% |

-2.85% |

||

|

-3 |

-18.00% |

0.92% |

-53.54% |

12.53% |

||

|

DJ 30 |

1 |

2.43% |

0.00% |

19.80% |

0.00% |

|

|

3 |

5.99% |

-0.43% |

46.33% |

-4.36% |

||

|

-3 |

-6.04% |

0.42% |

-33.49% |

8.64% |

||

|

Russell 2000 |

1 |

4.82% |

0.00% |

20.04% |

0.00% |

|

|

3 |

13.11% |

-0.45% |

36.45% |

-7.89% |

||

|

-3 |

-12.57% |

0.63% |

-44.70% |

5.14% |

||

|

MSCI Emerging |

1 |

1.85% |

0.00% |

12.37% |

0.00% |

|

|

3 |

4.32% |

-0.41% |

16.84% |

-6.76% |

||

|

-3 |

-4.83% |

0.24% |

-24.04% |

4.36% |

||

|

Gold spot |

1 |

0.71% |

0.00% |

18.09% |

0.00% |

|

|

2 |

0.53% |

-0.45% |

26.62% |

-4.78% |

||

|

-2 |

-0.76% |

0.33% |

-21.42% |

7.38% |

||

|

Silver stain |

1 |

14.38% |

0.00% |

28.46% |

0.00% |

|

|

2 |

28.39% |

-0.19% |

41.79% |

-7.57% |

||

|

-2 |

-25.66% |

1.55% |

-44.39% |

6.27% |

||

|

S&P Biotech Select |

1 |

2.06% |

0.00% |

6.23% |

0.00% |

|

|

3 |

3.49% |

-0.90% |

-16.81% |

-11.83% |

||

|

-3 |

-6.09% |

0.03% |

-37.79% |

-6.37% |

||

|

PHLX Semi-second. |

1 |

13.18% |

0.00% |

48.44% |

0.00% |

|

|

3 |

41.37% |

0.61% |

131.19% |

-4.71% |

||

|

-3 |

-31.54% |

2.67% |

-76.40% |

22.97% |

Click to enlarge

The bullish leveraged biotech ETF (LABU) presents the worst monthly and annual declines: -0.90% and -11.83%, respectively. The Leveraged Bearish Semiconductor ETF (SOXS) presents the highest monthly and annual positive drift: +2.67% and +22.97%, a significant loss.

A positive drift is accompanied by a consistent trend in the underlying asset, regardless of the direction of the trend and the direction of the ETF. This means that a positive drift can result in a gain or loss for the ETF. Negative drift is accompanied by daily volatility of returns (“whipsaw”). Whipsaw occurs more often in downtrends of the underlying asset.

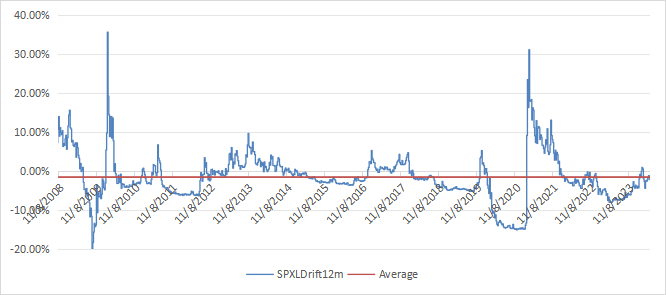

SPXL drift history

In the table above, SPXL shows a slight negative drift for both periods. The following graph traces its drift over 12 months since its creation (05/11/2008). The 12 months of pre-creation data used for the calculation are synthetic prices calculated from the daily returns of the S&P 500.

12-month drift of the SPXL since its creation. (Graphic: author; data: Portfolio123)

The average drift over 12 months over this period is negative: -1.63%. SPXL has suffered a decline since its launch, but the drift has been overshadowed by the uptrend: its total return is 3,813% (26.55% annualized).

The drift fell into negative territory during the March 2020 crisis. It surged to +31% in April 2021 after the stock market experienced one of its strongest rebounds in history, leading to significant positive slippage . While SPY has returned about 39% in a year, SPXL is up 162%. This is about four times the return of the underlying index, showing the upside of beta slippage in an uptrend. Then SPXL price action got scary between 03/01/2022 and 03/01/2023: it lost around 36% while SPY was down 6.7%, with leverage factor apparent close to 6 over this period!

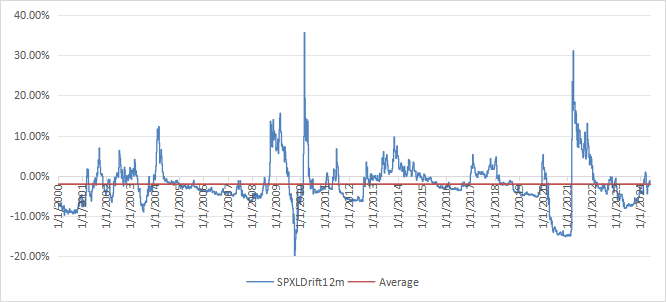

The performances simulated from January 2000 are worrying. Over this period, including two bear markets, the annualized return of the SPXL would have been lower than the index without leverage (4.36% compared to 7.34% for the SPY), with a maximum drawdown of -98%. This is a strong warning against a buy and hold strategy! The following graph represents the hypothetical 12-month drift from January 2000. The average is -2.14%.

Drift over 12 months since January 2000 (synthetic prices) (Graph: author, data: Portfolio123)

SPXL and other 3x leveraged ETFs are not long-term investments. They are trading and hedging instruments intended to be used for limited periods by seasoned traders who have a good understanding of their behavior. For hedging purposes, back 2x S&P 500 ETFs like the ProShares UltraShort S&P500 ETF (MSDS) are relatively more secure, although they can suffer significant degradation during very volatile periods (SDS history analysis).