News

Good, not great, news about inflation

Unlock Editor’s Digest for free

FT editor Roula Khalaf selects her favorite stories in this weekly newsletter.

This article is a local version of our Unhedged newsletter. Premium subscribers can subscribe here so that the newsletter is delivered every day of the week. Standard subscribers can upgrade to Premium hereor to explore all FT newsletters

Good morning. Stocks hit an all-time high high yesterday, passing through the March peaks. As a financial journalist, this makes me nervous. As an investor, this makes me happy. Tell me which one is right: robert.armstrong@ft.com.

CPI inflation: good enough for now

Every month Unhedged publishes a chart more or less similar to the one below. For the first time in 2024, we can do this without cringing:

Line drops! Good! After three months in which the monthly variation in core inflation was 0.4 percent, or an annualized rate well above 4 percent, the April figure was 0.3 percent, or 3.6 percent annualized. A significant improvement.

Why, then, didn’t the market seem to care more? Yes, two-year Treasury yields fell a respectable, if not precipitous, 9 basis points; shares rose more than one percent. But what hasn’t changed much are market expectations regarding a reduction in interest rates. Yesterday, the futures market expected cuts of 43 basis points by December. Today? 52bp. Oh yes.

What the market demonstrates is the difference between relief and surprise. There were good reasons to expect April’s numbers to be much better than those of the previous three months, and they were. But there were also good reasons to hope in February and March, and those hopes were dashed. Therefore, yields and stocks are showing relief. But the basic picture has changed relatively little. There were no major positive surprises that could change market forecasts for interest rates. Don Rissmiller of Strategas sums it up with characteristic impartiality: “The Fed has remained on hold and today’s inflation reinforces that decision.”

What the Fed wants most is for service prices to stop rising. But most of April’s improvements came in assets. In particular, the fall in car prices, both new and used, has accelerated, a trend that is expected to continue.

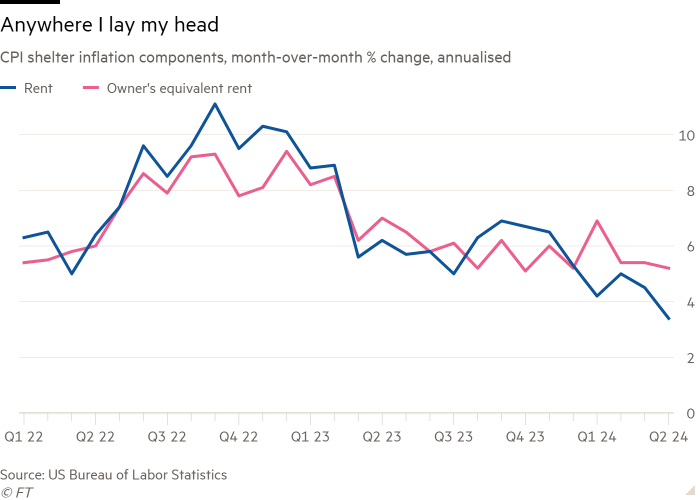

But there was also good news on the services side. Airfares continue to fall. Car insurance is still rising quickly, but not as quickly. And what really matters is the biggest and most watched service category of all: shelter. Rent fell significantly and equivalent rent to owners fell:

The movements may not seem impressive. And in fact, compared to measures of private renting that focus on new rentals, the CPI numbers still look terribly stark. But Omair Sharif of Inflation Insights sees reason for hope in the details. When seasonal adjustments to the index are removed, the trend appears more encouraging. And he points out that the Cleveland Fed’s New Tenant Rent (NTRR in the chart below) and All Tenant Rent (ATRR) indexes tend to lead the CPI rent in four and one quarters, respectively, and are pointing to new drops in rents in the months to come.

Reason for optimism, then. But it’s important to keep it simple. See the first graph above. April was an improvement, but it’s only one month and we’re still above the Fed’s 2% target. The multi-year averages are still well above the target. There is a way to go and the path will not be easy.

Gold and central banks

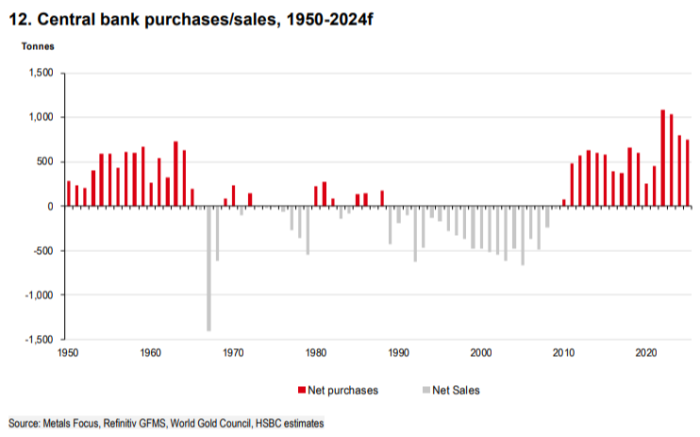

Yesterday I he wrote about the recovery in gold, which I still find difficult to justify in fundamental terms. Many readers wrote to point out that I had underestimated the change in central bank gold buying as a factor. They’re right. Here, from HSBC’s James Steel, is a long-term chart of global central bank gold purchases:

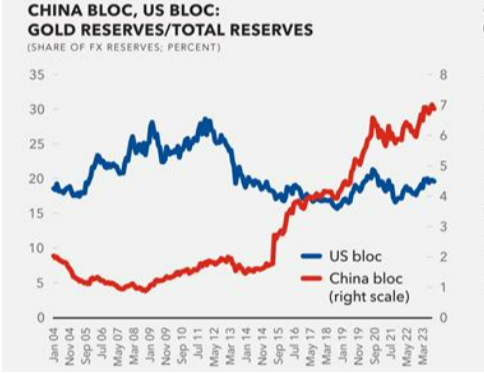

Banks have been buying around 400 tonnes a year since 2010, but in 2021 and 2022 they bought twice as much, and last year they were still at around 750 tonnes. What has changed? Joseph Wang, the central banking expert formerly known as Fed Guy, thoughts. Although the dollar remains the dominant currency in both global trade and global monetary reserves, “China bloc” countries have increased their gold holdings from very low levels to about 7 percent of total reserves. He borrows this graph from the IMF:

China’s own gold allocation is still very low compared to other countries, and its “buying spree” suggests it may be intent on changing that. Although in the years following 2008 China diversified its reserves, converting them into loans to countries it hoped to attract into its sphere of influence, it may be shifting towards gold, a process that could continue for many years. years.

Steel explains gold’s appeal to central banks as “a little more subtle than a simple de-dollarization story.” The dollar remains the dominant reserve reserve, but a shift of central bank portfolios to gold reflects a desire to diversify in some way. Monetary alternatives to the dollar (euro, pound, yen) are not particularly attractive; gold allows banks to diversify without buying it. And gold reserves can be mobilized to pay debts, resolve current account imbalances or avoid a currency crisis.

I am skeptical of stories about the end of the global order as we know it as justifications for any investment strategy. These things are very difficult to predict. But if central banks are constantly changing their allocations to gold, that’s more than just a story. There is just one problem. The violent jump in the price of gold this year, which surpassed the symbolically important $2,000 level, came well after the big increase in central bank purchases in 2022. Those who buy gold now may be following the central banks. But they also participate in a speculative frenzy.

A good read

FT podcast without coverage

Can’t get enough of Unhedged? To hear our new podcast, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Keep up with previous editions of the newsletter here.

Recommended newsletters for you

Swamp Notes — Expert views on the intersection of money and power in US politics. Sign up here

Due diligence — Top news from the world of corporate finance. Sign up here