ETFs

ETFs could capture half of current U.S. mutual fund assets, says Citi

Latest news on ETFs

Visit our ETF Center to learn more and explore our in-depth data and comparison tools

The fast-growing exchange-traded fund industry could take over half the money currently held by long-term U.S. mutual funds in the coming decade, according to Citi estimates.

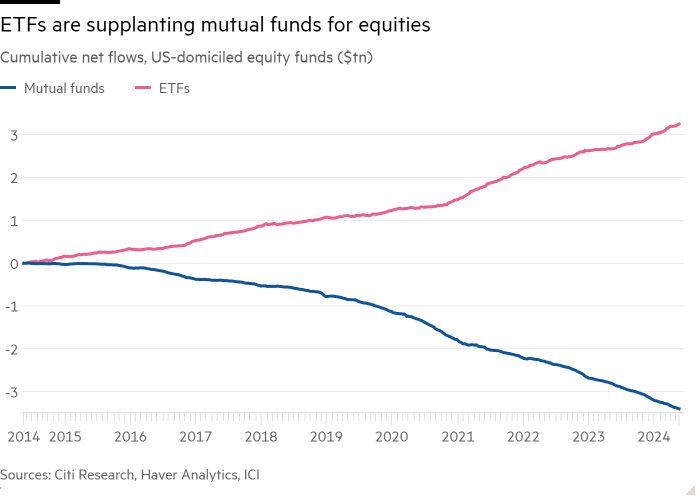

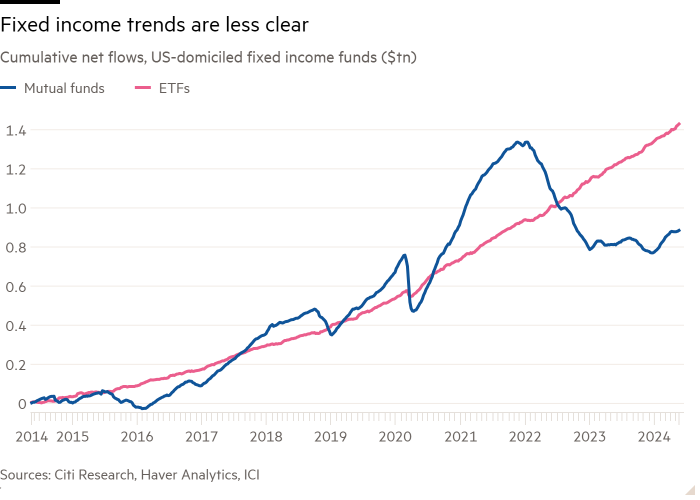

U.S. investors have been gradually moving away from mutual funds and toward ETFs for at least a decade, attracted by lower costs, better liquidity and greater tax efficiency. Mutual funds, excluding money market funds, have seen net outflows in nine of the past 10 years in the United States, according to data from the Investment Company Institute, even as ETFs have saved constant entries.

Despite this, the mutual fund industry remains much larger, with $19.6 trillion in long-term funds at the end of 2023, according to ICI, eclipsing the $8.1 trillion in state-listed ETFs -United.

However, this situation could reverse over the coming decade, according to Citi, which estimates that $6-10 trillion of the money remaining in long-term mutual funds is at risk of being captured by AND F.

“The U.S. asset management industry is clearly in an ongoing paradigm shift,” said Scott Chronert, global head of ETF research at Citi. “The flow trends speak for themselves.

“In total, we anticipate that between $6 trillion and $10 trillion in additional mutual fund assets under management are potentially at risk of being replaced or cannibalized by ETFs,” he added.

Mutual funds held outside of tax-exempt retirement accounts are most vulnerable to predation because they are unable to compete with many ETFs’ ability to defer capital gains taxes that accumulate within a fund.

Citi estimates that between half and all of the $2.4 trillion currently held by retail investors in non-tax-exempt mutual funds is a potential target for replacement by ETFs.

Additionally, between a quarter and half of the $4.1 trillion in equivalent money held by institutional investors, and as much as a fifth of the $1.3 trillion tax-free variable annuity market are also up for grabs.

Chronert pointed to the growing use of model portfolios, which are typically constructed using ETFs, as a key factor driving this trend.

The $11.9 trillion in mutual funds held in tax-exempt retirement structures, such as 401k defined contribution plans and individual retirement accounts, are likely to prove more difficult as ETFs do not benefit from any tax advantage in this area.

Nonetheless, Citi argued that there were a number of trends that would allow ETFs to reduce the dominance of mutual funds in this area.

First, IRAs represent a growing share of retirement assets in the United States, from less than 20 percent in 1995 to about 35 percent today.

This is relevant because even though “historically, ETFs have not had a place in the 401k menu,” IRAs “are generally much more open in nature than a fixed menu of funds,” meaning that ETFs ” certainly have a significant and growing opportunity. here,” Chronert said.

Mutual funds’ share of IRA assets has already declined by about 10 percentage points to 40 to 45 percent since 2005, Citi found.

Second, even within 401ks, more and more programs now offer a self-directed brokerage option, giving savers access to a much wider range of investments. ETFs now represent 23 percent of self-managed assets, up from 12 percent a decade ago.

Other opportunities abound. The vast majority of 401k savers under the age of 35 simply invest in a target date fund, designed to adopt an age-appropriate level of risk. FactSet research suggests that many of these target date funds in turn use ETFs to manage this upward trajectory.

Finally, Citi believes that demographics will play a role as younger generations – who show stronger preferences for ETFs – create assets.

Combining this, Citi estimates that 50% to 60% of the $7.4 trillion held by retail investors in retirement accounts could be captured by ETFs, as well as a small slice of the $4.5 trillion in institutional money and variable annuity rate.

Combined with its estimates for non-tax-exempt investments, this would mean that $6.3 billion to $10 billion of the $19.6 billion currently held by U.S.-domiciled mutual funds would be a potential target for ETFs.

But others saw things a little differently.

Bryan Armour, director of passive strategies research for North America at Morningstar, noted that in 2022 and 2023, “something like $1.6 billion has been withdrawn from mutual funds and a large part of that went to ETFs,” adding, “I don’t know if there are mutual funds. a natural point where [that flow] stop “.

However, Armor believes that mutual funds have some advantages over ETFs, such as the ability to reach out to new investors if a fund grows too large. He also saw use cases for assets such as private credit, which mutual funds can hold but ETFs cannot.

“The 800-pound gorilla in the room,” Armor said, is an opportunity for the Securities and Exchange Commission to approve asset managers’ many requests to copy the “ETF structure as a share class ” which helped propel Vanguard’s rapid expansion, the patent for which has now expired.

Obtaining approval would potentially make affected pre-existing mutual funds more tax efficient, easing pressure on investors to switch to an ETF.

However, when it comes to retirement plans, Armor believes that mutual funds are “under attack more from collective investment funds than from ETFs.”

CITs, which make up 38 percent of active 401Ks, according to ICI and BrightScope, “are cheaper to manage.” [than mutual funds] and they may have variable fees [meaning] they can negotiate lower fees for larger packages,” Armor said.

Research firm Cerulli Associates agrees with Armor on this point, arguing that the growing adoption of CITs in the DC market “has raised the question of whether mutual funds are heading toward obsolescence.”

“CITs have been gaining market share and are outpacing 401k mutual funds,” said Adam Barnett, principal analyst at Cerulli. “CITs, overall, have much lower management fees than mutual funds of similar composition.”