ETFs

ETFs buy nearly half in April as US rate cut hopes fade

Stay informed with free updates

Simply sign up to the myFT Digest of Exchange Traded Funds, delivered straight to your inbox.

Latest news on ETFs

Visit our ETF Center to learn more and explore our in-depth data and comparison tools

Investors reacted in April as prospects of falling short-term U.S. interest rates sparked widespread risk aversion, according to global data on exchange-traded fund flows.

However, signs of animal mood persisted in some segments of the global market, with solid demand for some cyclical assets, such as European and Japanese stocks and emerging market debt.

Overall, net flows into ETFs fell from $126.5 billion in March to a “muted” $68.5 billion in April, according to BlackRock data. Stock purchases fell even more sharply, from $106.3 billion to $40.7 billion, as demand for fixed-income ETFs – an inherently less risky asset class – rose to reaching $27.4 billion despite overall ETF flows cutting nearly in half.

Risk aversion was evident even within these bond flows, with government bond ETFs – again more of a safe haven than corporate bonds – bringing in $10.1 billion, the most high since October.

Moreover, even this demand for government bonds evoked a safety-focused mood, with flows into short-term (up to three years) U.S. Treasury ETFs turning positive for the first time since October and “intermediate » (from three to seven years old). -year) funds absorb most of the rest.

“We have more inflows in the upstream sector, and also midstream, than further down the sector. [yield] curve,” said Karim Chedid, head of investment strategy for iShares in the Emea region at BlackRock.

“It’s a matter of carrying. You can get good returns from the front and belly [due to the Treasury yield curve being inverted] and are less exposed to rate volatility,” he added.

Chedid summed up the mood in April as “mitigated risk rather than risk aversion” as markets fell amid further declines in expectations for Federal Reserve easing.

“In a general way [the flows data] is definitely weak for stocks. It was not a good month for risky assets in terms of stock performance. We’ve had significant pullbacks on rate expectations, particularly from the Fed,” said Chedid, who nonetheless saw early signs of improving sentiment in May.

Scott Chronert, global head of ETF research at Citi, noted that in the United States, fixed-income ETFs actually made more money than equity ETFs in April, at $15.2 billion. dollars compared to 14.1 billion dollars.

“US-listed ETF flows have slowed this month amid generally risk aversion. The underlying trends also suggest more cautious positioning,” Chronert said. “Fixed income led all asset classes, but gains were tilted toward commodities, shorter durations and Treasuries.”

Matthew Bartolini, head of SPDR Americas research at State Street Global Advisors, again focusing solely on the U.S. ETF market, noted that corporate bond ETFs saw net outflows in April (of 3 .3 billion dollars) for the first time this year.

Globally, however, there have been some positives. Flows into ETFs focused on emerging market debt – at the riskier end of the fixed-income spectrum – turned positive for the first time this year, according to BlackRock, with $2.7 billion in net purchases.

“We are seeing persistent capital outflows, but the situation has started to change,” Chedid said. He believes emerging debt could offer significantly higher returns without some of the traditional downside risks that come with it, arguing that the emerging world is less vulnerable to swings in U.S. monetary policy than during the famous 2013 taper tantrum.

European stocks also saw strong demand, with a third straight month of net inflows, of $3.1 billion, bucking the trend seen for most of last year.

Chedid believes the turnaround in confidence is due to expectations that the European Central Bank could start cutting rates before the Fed, which has helped European stocks outperform their U.S. counterparts so far this year.

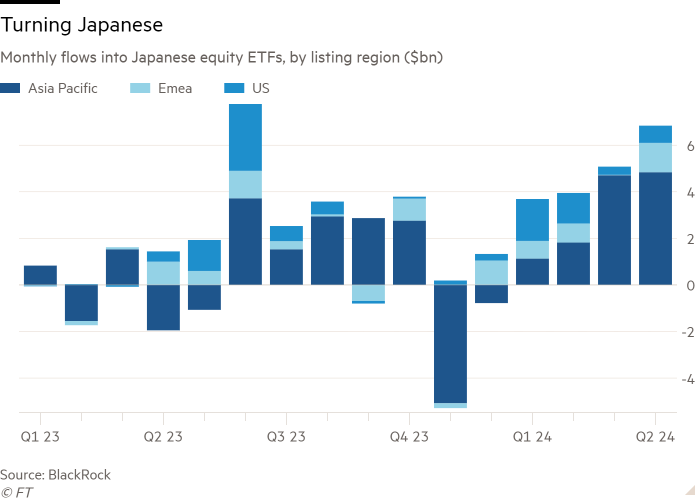

Japanese stocks are also in high demand, with April’s $6.8 billion in net buying being the second-highest monthly figure since the start of 2023 – even as the Bank of Japan ended its marathon stock buying spree. ‘s 14-year-old ETF purchases which allowed him to pocket 7 percent. percent of Japanese stock market capitalization.

Demand for Japanese stocks is evident among European and American investors, as well as in the Asia-Pacific region,

Chedid believed this was a structural trend that was set to continue, with Japanese stocks currently accounting for less than 2 percent of the average European wealth portfolio, compared to Japan’s current weighting of 5.3 percent in the MSCI All Country World Index.

Tying them together, Bartolini said U.S.-listed developed market ETFs excluding U.S. stocks recorded a 46th consecutive month of inflows in April, a trend he attributed to the use of ETFs as basic elements in asset allocation models, as well as “extended capital flows”. valuations in the United States and more favorable valuations abroad.”