DeFi

DeFi in 2024: new dynamics, challenges and opportunities

Explore the state of DeFi and the crucial changes the sector has undergone since the last bull run.

DeFi, or decentralized finance, was one of the key narratives of the previous market cycle.

The total value locked (TVL) in DeFi protocols increased from $1 billion in May 2020 to $260 billion by the end of 2021, before falling to the new base level of $60 billion during the bear market that followed. This figure began to increase with the new growth cycle, now reaching $156 billion (source: DeFiLlama).

However, this cycle differs from the previous one in many aspects, from the nature of the largest protocols to the blockchains they are built on. Understanding these changes can provide valuable insight into current risks and opportunities within the DeFi sector. But first, what exactly do we mean by DeFi?

DeFi protocols and their evolution

One of the first use cases for DeFi was lending-borrowing, with protocols such as Aave or Compound Finance allowing users to lend/borrow cryptocurrencies through a decentralized platform.

DEXs (decentralized exchanges) like Uniswap and bridges like WBTC have been developed to help users trade or transfer cryptocurrencies from one blockchain to another.

Decentralized stablecoins such as DAI (issued by Maker DAO) were created as a decentralized alternative to coins like Tether or USDC.

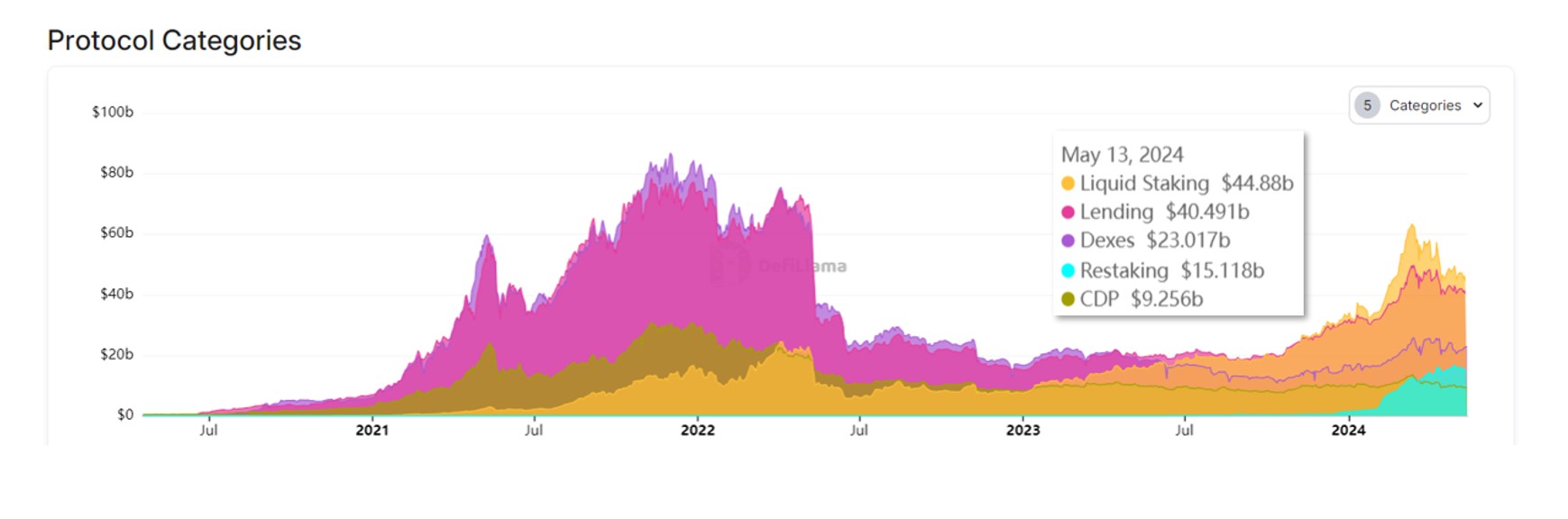

These three use cases were the largest in the previous market cycle, accounting for 30%, 32%, and 13% of TVL, respectively (TVL in bridges is not considered). The rest of the TVL was shared between derivatives, payments, and insurance protocols, as well as the burgeoning liquid staking category that would soon eclipse them all.

Indeed, with Ethereum changing its consensus from Proof-of-Work to Proof-of-Stake in September 2022, liquid staking has become the leading DeFi protocol. Liquid staking allows users to stake their coins in a PoS blockchain, while getting an IOU token in return, which they can use in other DeFi protocols (e.g., as collateral), thereby making their money grow twice . Lido, which offers liquid staking on Ethereum and Polygon, has become the largest in this category, now having over $27 billion in tokens staked.

As the new market cycle unfolds, the DeFi sector is growing alongside the broader crypto space. However, the composition of this sector is now completely different from that of 2020.

Liquid staking along with new retaking (offering yet another way to use already staked coins, like EigenLayer) now represents 38% of the total TVL. Lending DApps represent 26% of TVL, DEXs 14%, and decentralized stablecoins 6%.

Why is composition important? It could be argued that the value proposition brought by liquid staking and re-staking protocols to the space is less than that offered by the first “wave” of DeFi DApps. Not to mention “liquid restocking” and other complex constructions on top of the coins already in circulation. This situation could suggest some stagnation within the sector, especially since a large number of new TVLs come from similar protocols built on new blockchains.

DeFi Blockchains

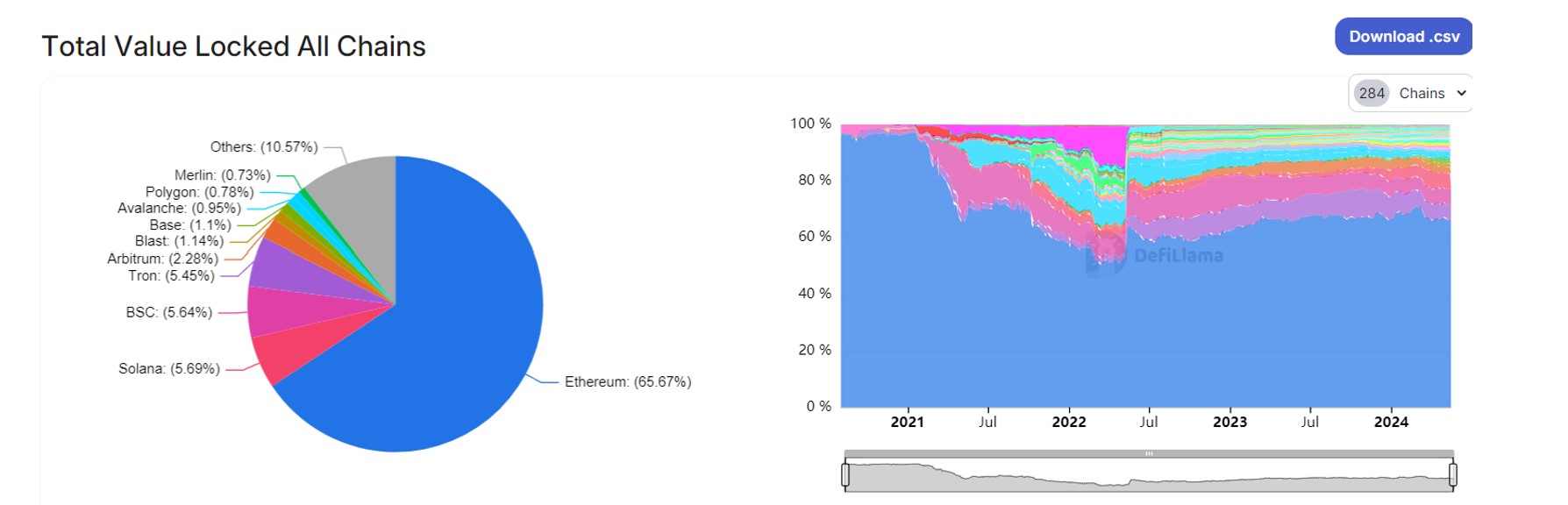

In 2020, 96% of TVL was recorded on Ethereum alone. Today, Ethereum’s share is only 66%, which is still a lot but shows that other blockchains are emerging.

Solana, BSC and Tron are now each seeing over 5% TVL, actively developing their own DeFi ecosystems. Additionally, with new layer 2 developments on Bitcoin, we may also see Bitcoin-based DeFi protocols emerge in the future.

Increasing diversity is generally a good thing, but in the case of DeFi it shows space replicating the same ideas within different blockchains instead of innovating.

What prospects for DeFi?

Innovators can explore several avenues, and the most obvious is probably RWA, or tokenization of real-world assets. The basic assumption here is that absolutely any asset can be tokenized and traded without the obstacles imposed by traditional finance. This is a huge market, one that Citi estimates will reach $4 trillion by 2030 and could boost DeFi in several ways.

However, the current TVL of decentralized RWA protocols hovers modestly around $6 billion, with the protocols primarily tokenizing US dollars, treasuries, and real estate. Such slow development could be attributed to significant regulatory gaps, particularly in the United States. In the EU, the MiCA regulation also does not directly cover DeFi, keeping the DeFi sector in limbo.

Another issue is the continued exploits that still plague the sector, but this could be resolved through technological advancements and DeFi insurance – yet another avenue of innovation to explore.