Fintech

Dave is an undervalued fintech with EPS potential of over $10 in 2025 (NASDAQ:DAVE)

Dedual images

Dave Inc. Background History

Dave Inc. (NASDAQ:Dave) is a fintech company founded in 2016 by Jason Wilk. The company launched the Dave app in 2017. The company raised venture capital in 2018-2021. The company went public in late 2021 via a merger with a SPAC, VPC Impact Acquisition Holdings III, which valued Dave at $4 billion. Despite having a healthy profit margin of around 10-20% for most of its life as a private company, after going public, Dave increased spending on marketing and customer acquisition, which caused large losses in 2022 and 2023, masking the company’s strong unit economics. Management has started to pull the levers for profitability in 2023 and the results are starting to show now. There is significant upside to earnings estimates as the company continues to drive profitable growth. Specifically, management is testing a new subscription price of $4/user/month for all customers using Dave’s core cash advance product. By my estimates, this change alone has the potential to drive the company’s EPS to over $10/share in 2025 or 2026 versus consensus EPS of $2.10 in 2025. In my base case, with no change to the subscription price, I estimate Dave will earn $3.11 in EPS, which is still 50% above the stock. I estimate the stock to be worth over $100/share in the next 12-18 months as the market wakes up to Dave’s earnings power and enterprise value.

How the business works

Dave’s main product is a $25 to $500 cash advance, which is used by U.S. consumers to avoid overdraft fees and make ends meet. The company serves underserved consumers who often turn to expensive check-cashing loans or short-term loans. There are three methods consumers can use to borrow from Dave: first, instant on the Dave card which has a 3% fee, plus Dave earns interchange on transactions which averages about 2%. Second, directly to a bank account with Visa Direct, which has a 5% fee. Finally, via ACH transfer to a bank account, which is free. Dave does not charge interest on its cash advances, just the initial transfer fee for extra speed, similar to the revenue model Venmo and CashApp charge for fast delivery. Dave has 2.2 million monthly active members who average three transactions per quarter for a total of 6.6 million transactions per quarter. The average origination size is $159 and the average transaction revenue is $9, a withdrawal rate of 5.7%. Additionally, Dave makes money through tips and subscriptions. Cash advances are automatically refunded from the consumer’s bank account as soon as their paycheck hits the account. Dave’s credit losses are about 1.3% of originations because of the way they extend extra cash products. Dave starts with a $25 advance. If that amount is refunded multiple times, they will gradually increase it over time, up to a maximum of $500. The average length is only 14 days, so the velocity of the advances is very high, allowing Dave to adjust his credit model in real time.

Dave competes with companies like Chime, MoneyLion, and Brigit. Chime is expected to IPO in 2025, which will lead to more understanding of the cash advance business and another comparable company. Chime last raised capital in 2021 at a valuation of $25 billion.

Dave is an early adopter of AI, using it both in its credit models to determine which consumers get cash advance offers and for how much, and in its call centers, resolving 90% of tickets without contacting an agent. These results allow Dave to offer better customer service and a lower price than its competitors.

The Path to $10+ EPS

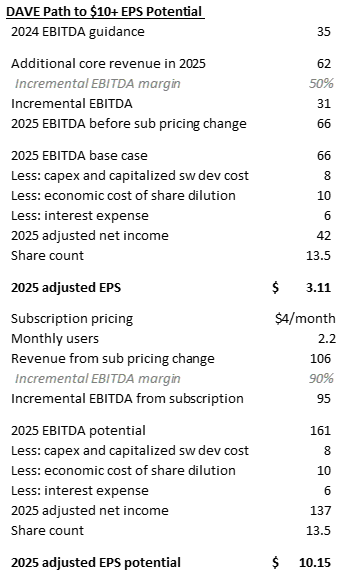

Until the last few months, Dave had no sell-side analyst coverage and few investors understood Dave’s business model and potential. Consensus estimates have not reached the level of profitability that Dave is on track to achieve. I estimate that in my base case, Dave will earn $3.11 in EPS. And it has the potential to earn over $10 in EPS in 2025 or 2026 with the subscription pricing change they are testing and will likely launch later this year.

As discussed in the last earnings call, Dave has implemented a new billing system and is testing new subscription pricing. I estimate that Dave could implement pricing of $3-$5/month for all of their monthly users. At that price, it’s still a significant discount compared to competitors like Brigit who charge over $10/month in subscription fees.

I estimate a 50% incremental EBITDA margin on core business growth, which is lower than the 150% incremental margin DAVE has generated over the last five quarters. The incremental revenue stream has been above 100% because Dave has reduced the level of marketing and opex spend.

Additionally, I estimate that Dave will generate $4/month on its 2.2M monthly active users, generating an incremental $106M in revenue at a 90% margin. This brings its 2025 EBITDA potential to $161M, versus $51M for the Street (the Street is not modeling the change in subscription prices).

From there, removing capex and capitalized software development costs, economic cost of dilution, and interest expense gives $137 million in adjusted net income. Divided by 13.5 million diluted shares, we get $10.15/share in adjusted EPS (economic earnings). The company will not pay taxes for many years, given the large NOL balance. Note that stock-based compensation in the GAAP financials is based on equity awards granted at the time of IPO at $320/share. I calculate economic dilution by looking at market cap x annual percent dilution from there, which comes out to $400 million x 2.5% = $10 million/year.

Business orientation and my estimates

Assessment

In my base case, I estimate Dave is worth $3.11 x 16x P/E = $50/share. However, if Dave executes the subscription price change, I estimate Dave is worth well over $100/share based on $10.15 EPS and at least a 10x P/E. Dave is currently trading at 14.2x, 2025 P/E. Applying the same earnings multiple to my 2025 EPS estimate yields a value of $144/share.

At $100, Dave would be valued at around $1.4 billion, significantly higher than its current valuation but still significantly below the $4 billion valuation that venture capitalists invested in the company in 2021 and its $4 billion IPO valuation, despite Dave having significantly grown revenue and led the company to software-like margins above 30%.

Looking at value from a different perspective, consumer finance companies spend hundreds of dollars per user to acquire new users. Dave has 10.8 million lifetime memberships and 2.2 million monthly active users. At $150 per lifetime customer membership, Dave is worth $1.6 billion, or $120/share. A strategic acquirer like Capital One or Citi might be interested in acquiring Dave and using Dave’s data on actual repayment history to make credit card offers to highly engaged consumers. Credit card products are much more profitable than cash advance. Over time, if Dave is not acquired, the company could launch its own credit card or credit origination product.

Risks

- Dave may not realize the earning power I expect because they may not change the price of the subscription. Or consumers may use Dave less frequently if there is a price change.

- Dave addresses credit risk. While credit metrics have improved significantly in recent quarters, a weaker consumer could lead to more delinquencies and more credit losses.

- Potential Regulatory Change. While Dave has never had any regulatory issues, the CFPB or other regulators could further regulate the cash advance industry, which would impact the entire industry, including Dave.