Fintech

Bancorp Stock: Fintech Solutions Push Bank to New All-Time Highs (NASDAQ:TBBK)

AsiaVision

Banca Popolare di Milano (NASDAQ:TBBK) is heading towards an all-time high and does not appear to be affected by the current macroeconomic environment. As expressed in my latest articleThis bank is not like the others, in fact it places a lot of emphasis on the fintech segment. In a certain sense, we could almost call it a tech-bank, in fact its profitability ratios are quite high. At the same time, it does not issue dividends to reinvest capital in its business, which is not very typical for a bank.

Thanks to its diversity, TBBK is performing very well this year (+35% YTD) and is poised to hit new all-time highs.

Q2 2024 Highlights

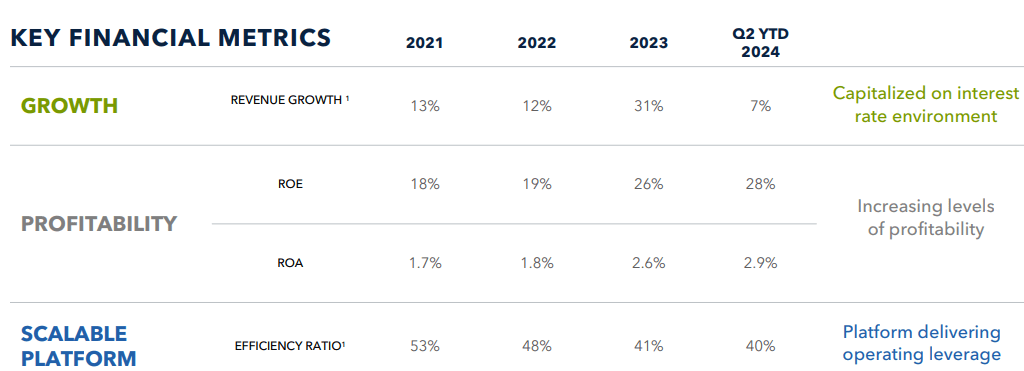

TBBK Quarterly Report It has been positive in more ways than one: there has been solid growth, profitability and business efficiency have improved.

TBBK Q2 2024

Revenues grew by 7% compared to Q2 2023, ROE and ROA reached 28% and 2.90% respectively. In addition, the efficiency ratio improved further and reached 40%. This is an exceptional result, made possible by revenues growing faster than non-interest expenses. In this case, it helped to leverage greater operating leverage through the fintech segment.

TBBK Q2 2024

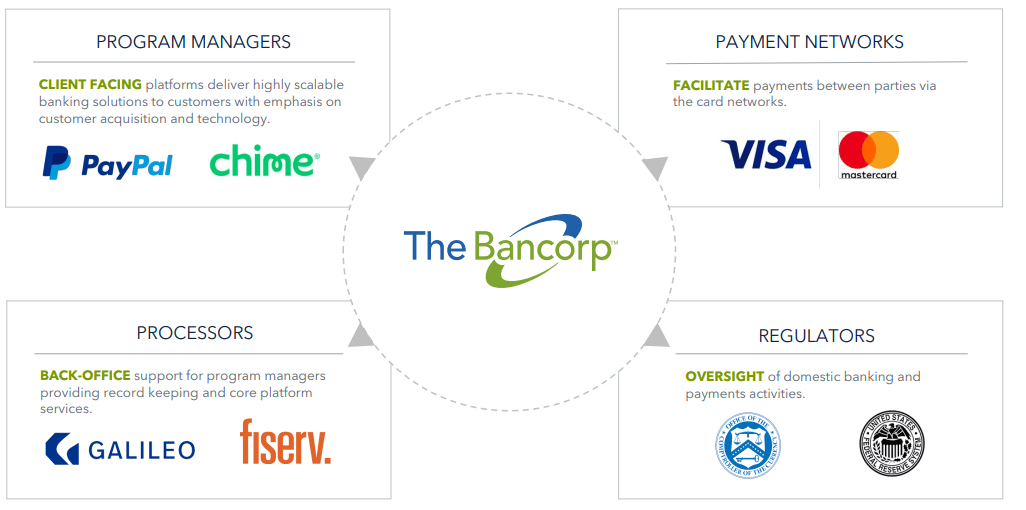

Over the years, TBBK has surrounded itself with leading companies in the payments sector and, to date, non-interest income is responsible for 22% of revenues. This is a very high figure and has implications not only in terms of earnings. In fact, fintech solutions tend to attract new stable and low-cost deposits.

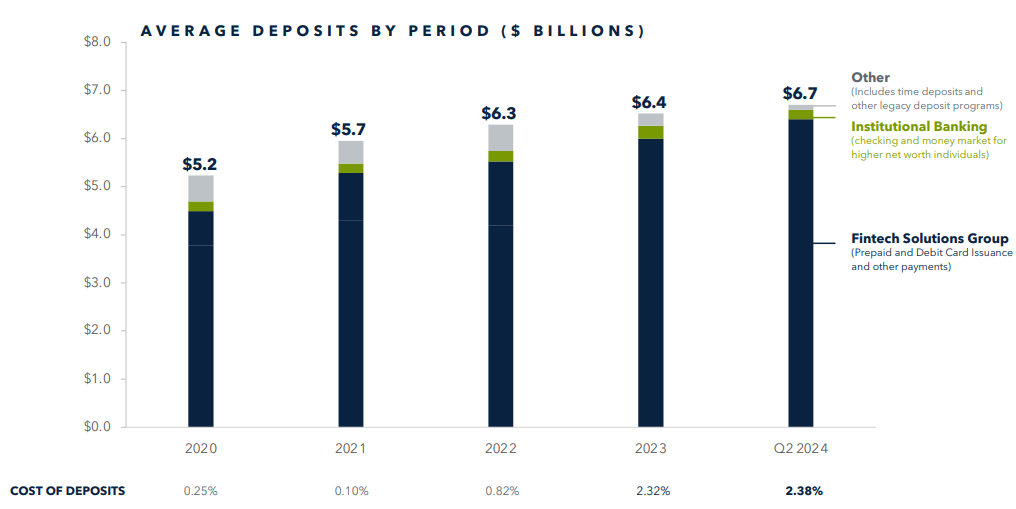

TBBK Q2 2024

A large percentage of deposits come from Fintech Solutions Group, and only a small percentage are time deposits and money market deposits. The average cost of deposits is not surprising, very low, only 2.38%. There are currently banks that are struggling much more and can not get below 4%; TBBK has basically stabilized the average cost well below 3%. By the way, 93% of deposits are insured, so below the threshold of $ 250,000. This is a sign of strong solidity for the deposit base because it implies a high granularity and diversification of customers. In such a situation the bank has a dominant position, since a small customer has no bargaining power and has to settle for lower interest on his account.

Being able to finance at a low cost is a huge advantage for a bank, because it can obtain a higher spread on its loans.

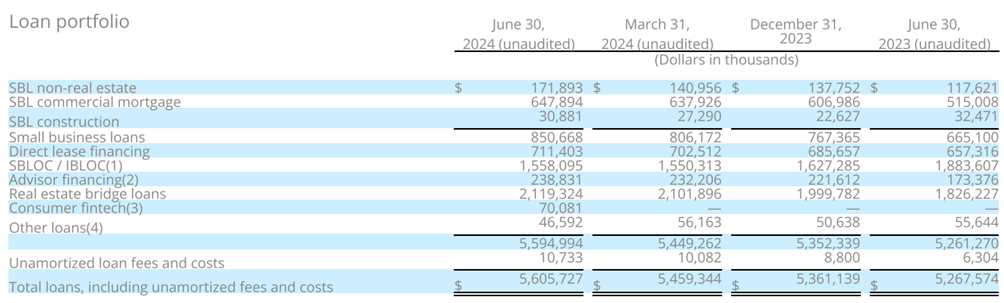

TBBK Q2 2024

As compared to Q2 2024, Total loans reached $5.60 billion, up 6.46% from last year. At first glance, this may seem like a disappointing result, but net interest income in the first half of 2024 reached $188.21 million, up almost 9% from last year. This means that the cost of deposits increased more slowly than the yield on loans. In addition, the net interest margin this quarter reached 4.97%, up 14 basis points from the second quarter of 2023: it is very rare to find a bank with a better result.

In all this, the only negative note is probably the increase in non-performing assets to total assets. Last year this ratio was 0.47%, today it is 0.95%, practically double. It is not yet a worrying level, but it should stop there.

Fintech solutions generated $55 million in revenue in the first half of 2024, up 10% from the previous year. The main drivers were an increase in transaction volume (up 13% from Q2 2024) and collaboration with new partners.

This business segment is growing at double digits and potentially offers large profitability as it is scalable.

TBBK Q2 2024

Management’s long-term plan is for TBBK to become a kind of technology bank. The core business will always be lending money, but financial technology will play such a major role that it will disrupt the financial results. From a long-term perspective, TBBK could have a ROE of more than 40%, a ROA of more than 4%, and an efficiency ratio of less than 40%.

While these targets may seem overly optimistic at the moment, management is actually slowly coming around and the market is increasingly accepting their vision. If it succeeds, I doubt many other banks could compete on profitability.

TBBK Q2 2024

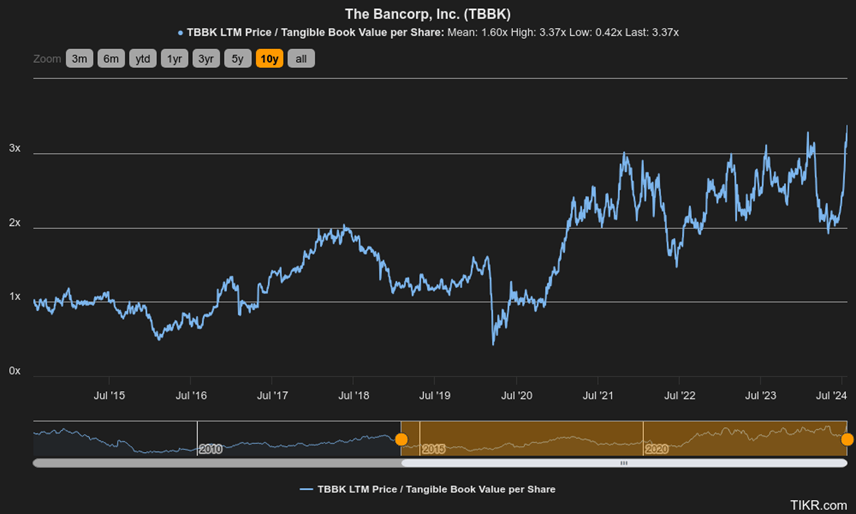

TBBK’s earnings per share look more like a technology company than a bank, but that’s precisely why this bank is trading at 3.37 times TBV per share.

TikR

Personally, I find the current valuation too high, which is why I consider TBBK a hold. However, I have no doubt that this bank deserves to be traded at higher multiples. The fintech segment is growing at double digits and has a lot of room for improvement in terms of profitability, so it would not be fair to price TBBK as if it were a traditional bank. At a price/TBV per share of 2x it could prove to be a reasonable choice, and just a few months ago it was at those prices.

Conclusion

TBBK is a very solid bank that is growing rapidly due to its exposure to the payments market. This bank is not like other banks; it has the traits of a technology company.

TBBK Q2 2024

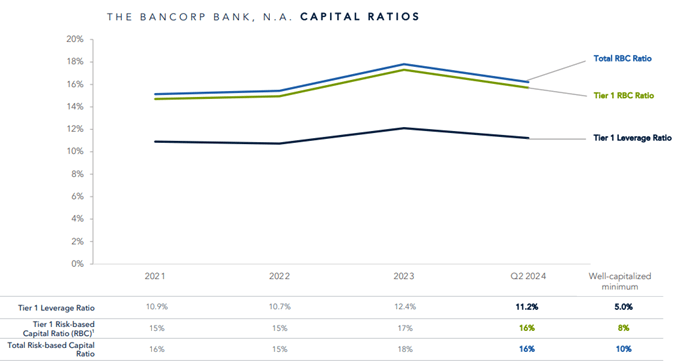

Looking at capital ratios, we see another difference compared to traditional banks, namely a risk-based capital ratio of 16%, which is very high and conservative despite many share buybacks in the past.

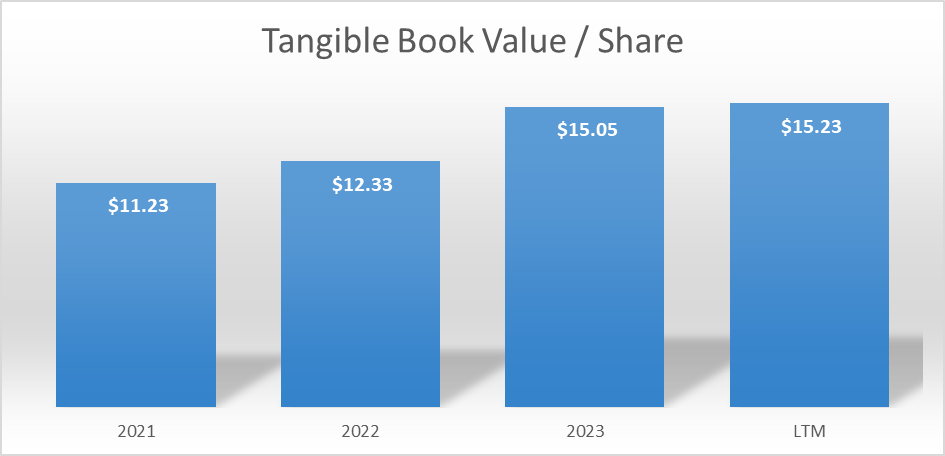

Chart based on SA data

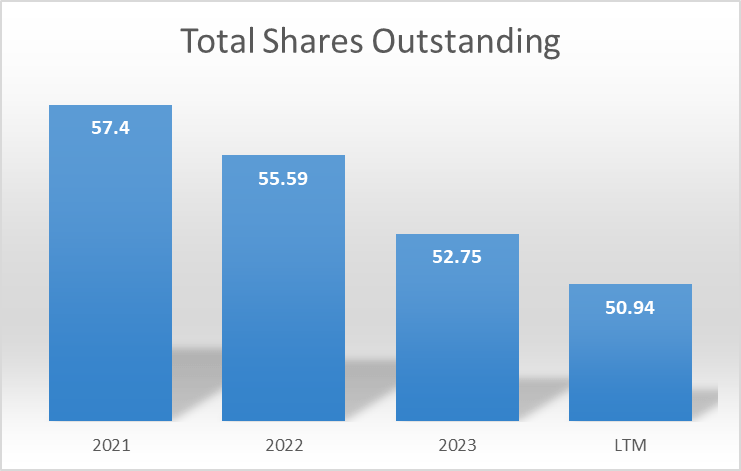

Since the end of 2021, shares outstanding have decreased by 11.25%, a significant and unusual figure for a bank. Consider that the repurchase entails a decrease in equity, a crucial factor in the valuation of any bank. Therefore, to repurchase so many shares, management must be firmly convinced of the bank’s financial position and its ability to increase TBV per share.

In Q1 2024, $50 million of treasury shares were purchased, in Q2 $100 million. In Q3 and Q4, another $50 million will be allocated each quarter.

Chart based on SA data

Management has been right so far, as TBV per share has grown year after year. Not even the rapid increase in interest rates has worried the solidity of this bank, as unrealized losses are negligible.

From a certain point of view, one of the advantages of this bank is that it does not issue dividends. While for some this may be a disincentive to invest in it, for others it is not at all, as they can take full advantage of compound interest. Profits that are not distributed are kept within the company, thus increasing the equity. At the same time, a portion can be reinvested to improve future revenue growth. In addition, buybacks versus dividends are a more tax-efficient way to reward shareholders.

In short, those who want to invest in TBBK should keep in mind that this bank is managed differently from a traditional bank, but these differences are the reason why it is trading almost at an all-time high today: many other peers have not even recovered from the collapse triggered by the failure of SVB. Of course, the opposite argument also applies, namely that it can collapse more than a traditional bank if fintech solutions stop its growth. After all, when a company uses operating leverage, it can encounter serious difficulties in times of recession.