ETFs

3 Solid, Little-Known Income ETFs

mevans/E+ via Getty Images

In this article, I’ll give a brief overview of three solid, but little-known, income ETFs. These each have fewer than 1,000 subscribers and receive very sporadic coverage from Seeking Alpha writers.

First up, we have the FolioBeyond Alternative Income and Interest Rate Hedge ETF (RISR). RISR focuses on interest-only MBS, negative duration securities. It has a dividend yield of 7.2% and a duration of minus 5. RISR’s high dividends ensure positive carry/expected returns in the long term, while its negative duration means the fund can be used to cover the bond holdings of an investor.

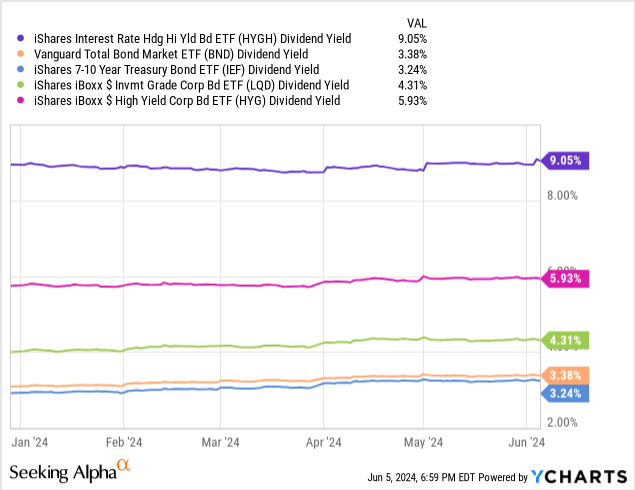

Second, we have the iShares Interest Rate Hedged High Yield Bond ETF (HYGH). HYGH invests in high-yield corporate bonds and hedges its interest rate risk using swaps. It has a dividend yield of 9.1% and effectively has zero interest rate risk. This seems like a particularly good choice right now, given how interest rates are moving.

Third, we have the Panagram Bbb-B Clo ETF (CLOZ). CLOZ invests focusing on BBB-BB CLO debt tranches, high yield investments with low credit and interest rate risk. CLOZ has a dividend yield of 9.3%, with effectively zero interest rate risk. Credit risk is much lower than HYGH, although liquidity risk is higher and volatility may increase during particularly severe recessions.

In my opinion, the three ETFs above are all solid investment and buying opportunities.

RISR – High Yield Negative Duration ETF

Strategy and participations

RISR explains everything about the fund, its holdings and its strategy in this document. fantastic pitchbook. I’ll give a brief overview myself, but the pitchbook explains everything well.

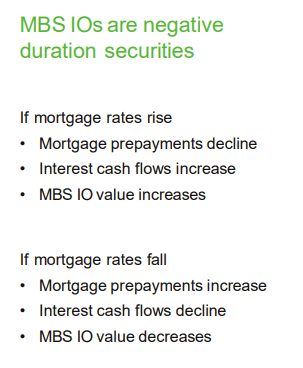

RISR focuses only on interest MBS. Simply put, these are mortgage consolidations, the homeowners pay the mortgages, the RISR only receives the interest payments. Other investors receive the capital payments.

Prepayment tends to hurt these securities because homeowners stop paying interest when they prepay their mortgage/the prepayment is just the principal. Prepayment is negatively impacted by tariffs. Higher rates mean homeowners would be forced to pay much higher mortgages if they moved. millions remain behind. A rate cut would have the opposite effect.

As a result of the above, interest-only MBS see prices and revenues decrease when rates decrease, and prices and revenues increase when rates increase. In the fund’s own words:

RISR

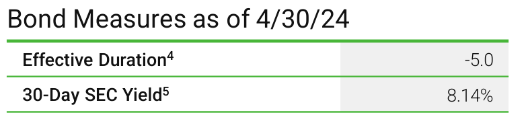

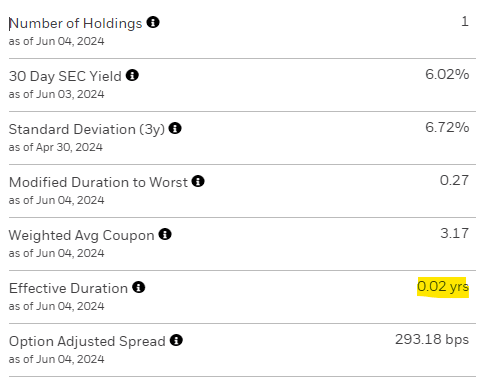

RISR itself sports a duration of minus 5, as expected.

RISR

Thesis on benefits and investment

RISR offers investors two key advantages: high dividends and simple interest rate hedging.

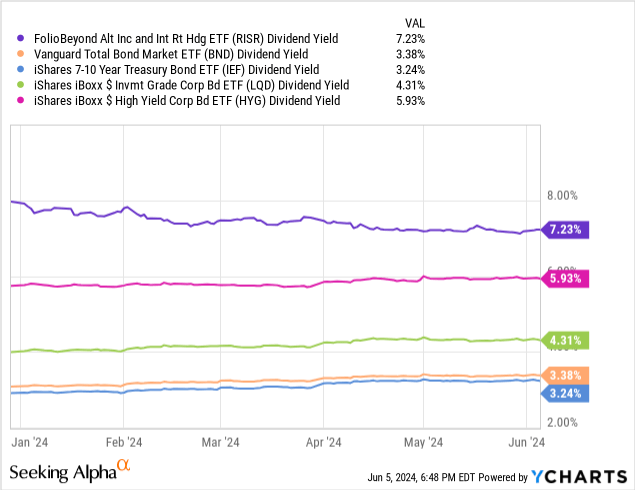

RISR’s strong dividends seem pretty self-explanatory: the fund yields 7.2%, more than most bonds and bond sub-asset classes.

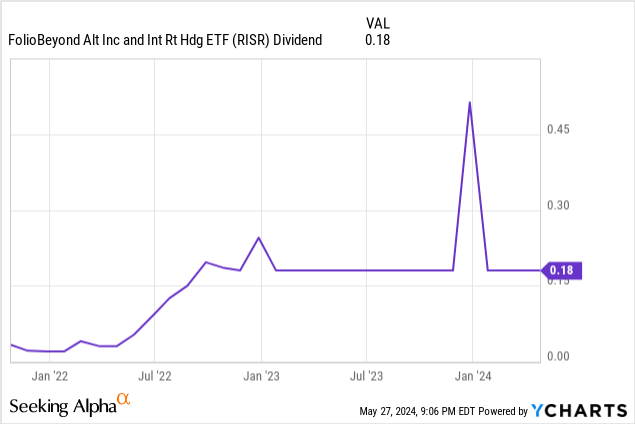

Data by YCharts

RISR’s dividends have seen strong growth since its inception, almost entirely due to Fed rate hikes. The peak at the end of 2023 was a particular end-of-year distribution.

Data by YCharts

The negative duration of RISR means that it can be used as a simple and effective interest rate hedge at the portfolio level. As an example, investors in the iShares 7-10 Year Treasury Bond ETF (IEF) can combine IEF with RISR to reduce their interest rate risk. Adjust the weightings and interest rate risk can be minimized. This should also lead to reasonably good returns, due to their high yields.

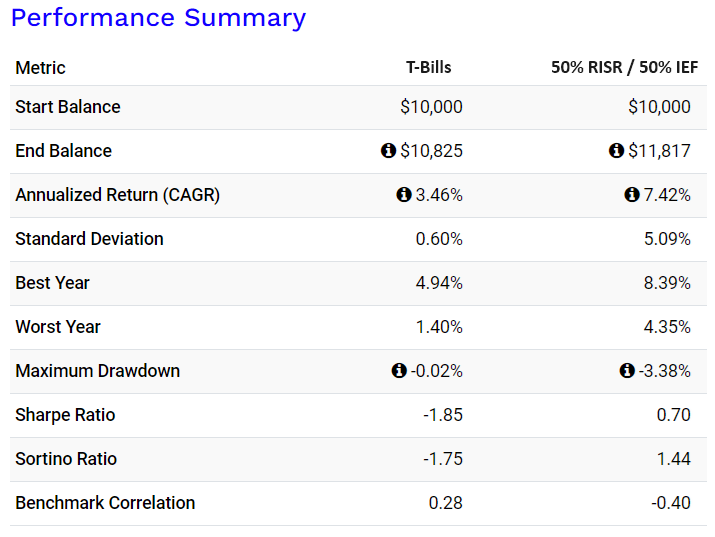

According to Portfolio Visualizer, a 50% RISR / 50% IEF portfolio would have significantly outperformed Treasuries in recent years. Risk-adjusted returns would also have been higher, but with greater losses.

Portfolio Viewer

In my opinion, and taking into account the above, RISR is an effective interest rate hedge at the portfolio level and using it as such is a great idea. Due to problems with convexity and the risk of prepayment, I would reduce any RISR investment somewhat.

By the way, duration is currently minimized with a 60% RISR / 40% IEF portfolio. I went with 50%/50% for the above as cash durations were higher in the past.

Performance history

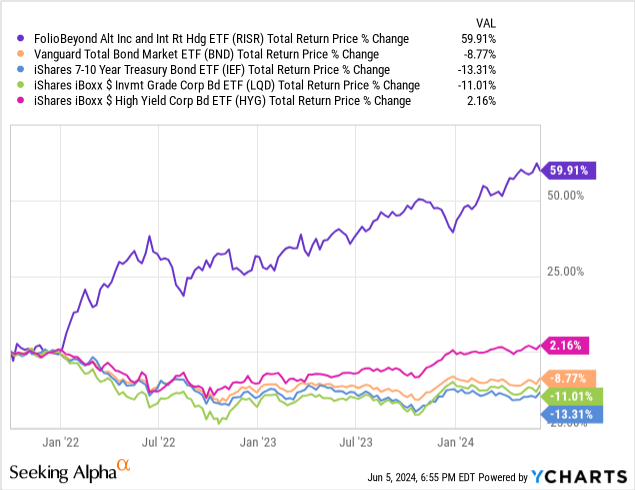

RISR’s performance history is beyond excellent, with the fund significantly outperforming all bonds and bond sub-asset classes since inception.

RISR’s outperformance is almost entirely due to its negative duration, with its above-average dividends playing a small, but positive, role.

I last covered RISR here.

HYGH – Hedged High Yield Bond ETF

Strategy and participations

HYGH invests in high-yield corporate bonds and hedges its interest rate risk using swaps.

The fund’s exposure to high yield bonds is indirect, through an investment in the iShares iBoxx $ High Yield Corporate Bond ETF (HYG). HYG’s fees are waived, with HYGH itself boasting an expense ratio of 0.52%, a bit higher than average for an ETF, but about average for a smaller, niche ETF.

The fund’s interest rate swaps reduce its duration to effectively zero. Credit risk remains the same: high and above average.

HYGH

Thesis on benefits and investment

HYGH has a dividend yield of 9.1%, quite solid on an absolute basis and higher than most bonds and bond sub-asset classes.

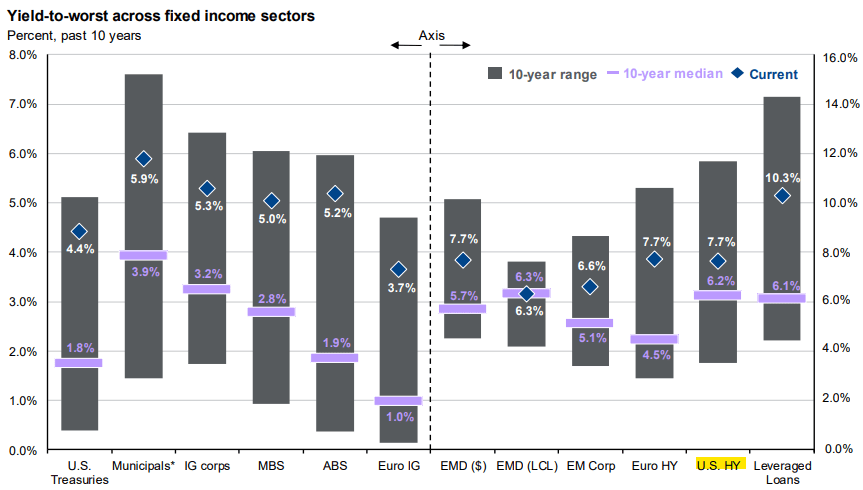

In some cases, ETFs must distribute gains from options and swaps to shareholders. Thus, the distribution yields of these ETFs do not necessarily reflect the underlying income generation. In the specific case of HYGH, it appears that high yield corporate bonds are currently yielding around 7.7%:

JPMorgan Markets Guide

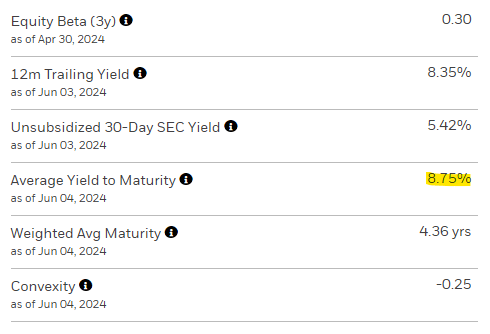

While the underlying securities of HYGH have a yield to maturity of 8.6%:

HYGH

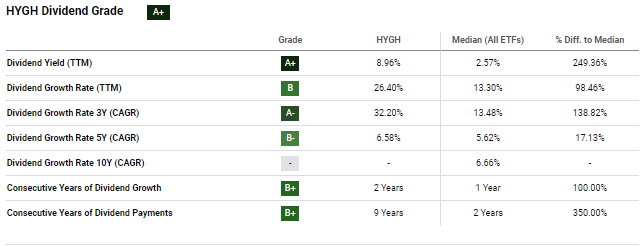

Considering the above, it appears that HYGH’s 9.0% dividend yield is mostly covered by underlying revenue/profits, but around 1.0% of it is not. .

Dividends have seen very healthy growth in recent years as Fed rate hikes have led to higher bond yields and gains on interest rate swaps.

In search of Alpha

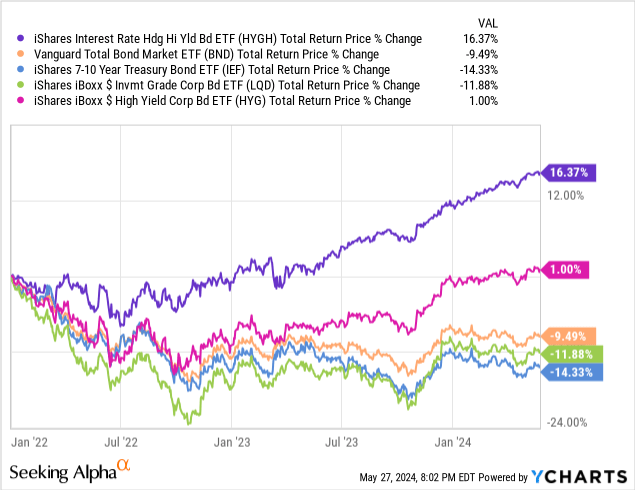

HYGH’s interest rate swaps effectively eliminate the fund’s interest rate risk. As a result, the fund tends to outperform when rates rise, as has been the case since the start of 2022.

Data by YCharts

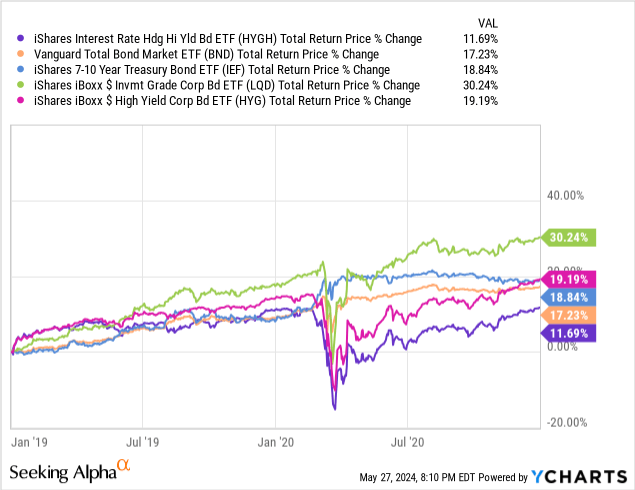

On the other hand, the fund tends to underperform when rates fall, as was the case from 2019 to 2020.

Data by YCharts

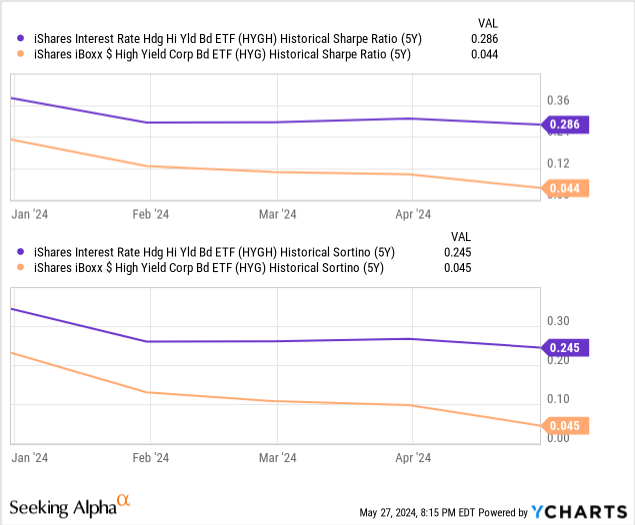

HYGH’s zero interest rate risk reduces portfolio risk and volatility over the long term, a clear benefit for investors. Expect higher risk-adjusted returns than high-yield corporate bonds, as has been the case over the past five years.

Data by YCharts

Performance history

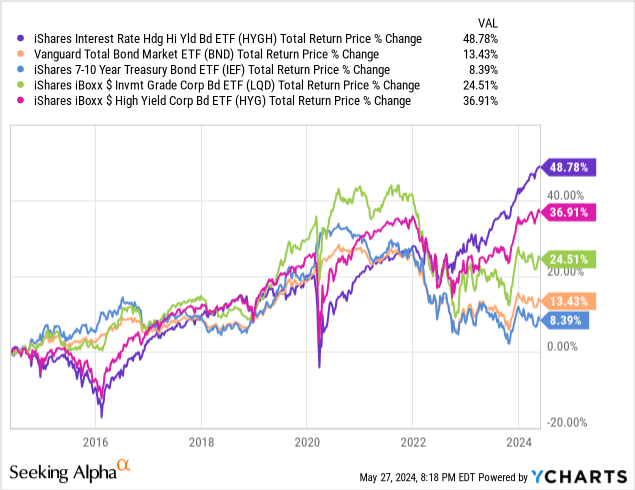

HYGH’s performance history is reasonably good, with the fund outperforming most bonds and bond sub-asset classes since inception. The outperformance is almost entirely due to the fund’s low rate risk, concentrated from 2022 onwards.

Data by YCharts

I last covered HYGH here.

CLOZ – CLO Debt ETF

Strategy and participations

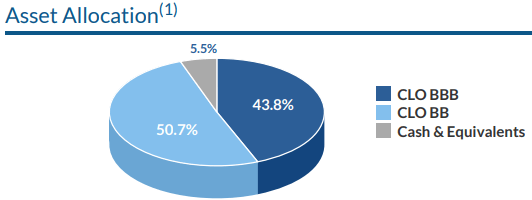

CLOZ invests in BBB-BB CLO debt tranches. Simplifying things enormously, we can say that the fund invests in batches of corporate loans (senior loans) and earns income from them. Current holdings are as follows:

CLOZ

Thesis on benefits and investment

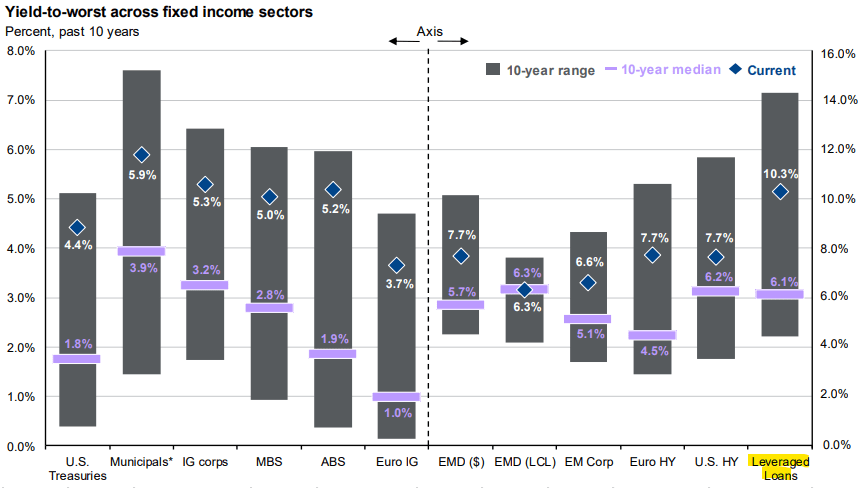

CLOs are backed by senior loans, which currently constitute the most profitable investments.

JPMorgan Markets Guide

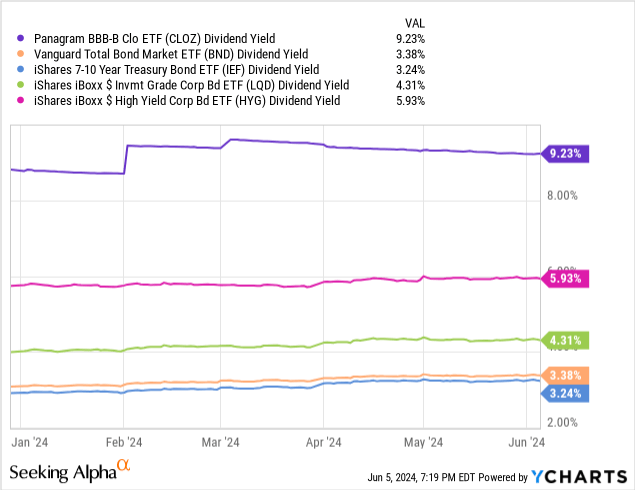

CLO debt tranches also boast high yields, with CLOZ currently yielding 9.2%, more than almost all bonds and bond sub-asset classes.

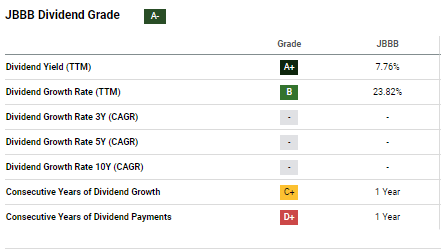

Dividends should also have seen strong growth, but with inception in early 2023, the fund is too young for us to meaningfully analyze its dividend growth track record. CLO debt tranches have certainly seen higher coupons thanks to higher rates, with other CLO debt ETFs seeing positive dividend growth. These include the Janus Henderson B-BBB CLO ETF (JBBB), quite similar to CLOZ.

JBBB

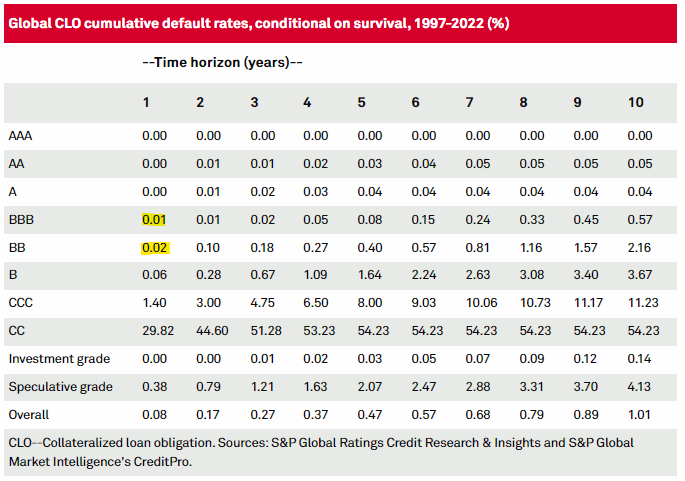

CLO debt tranches have extremely low default rates, ranging from 0.01% to 0.02% per year. Default rates rise during downturns and recessions, and could spike during particularly bad times. In my opinion, the credit risk for these securities is higher than these numbers suggest, but still low/moderate.

S&P

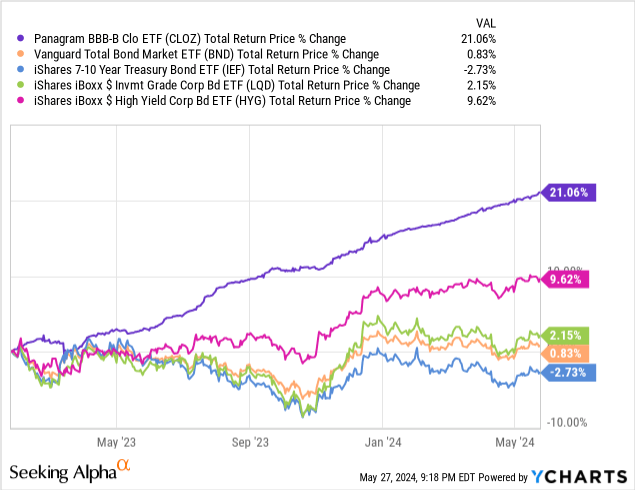

CLO debt tranches are floating rate investments with negligible interest rate risk and duration. Expect the fund to outperform when rates rise, as it has since its inception.

Data by YCharts

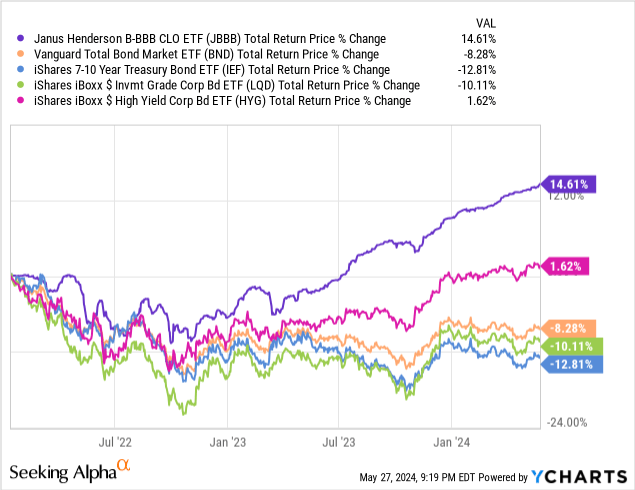

JBBB has also outperformed since the start of 2022, a longer and more significant period than CLOZ.

Data by YCharts

CLO debt tranches sometimes experience higher volatility and drawdowns than expected. In my opinion, this is due to liquidity issues and the fact that investors perceive these investments to be quite risky.

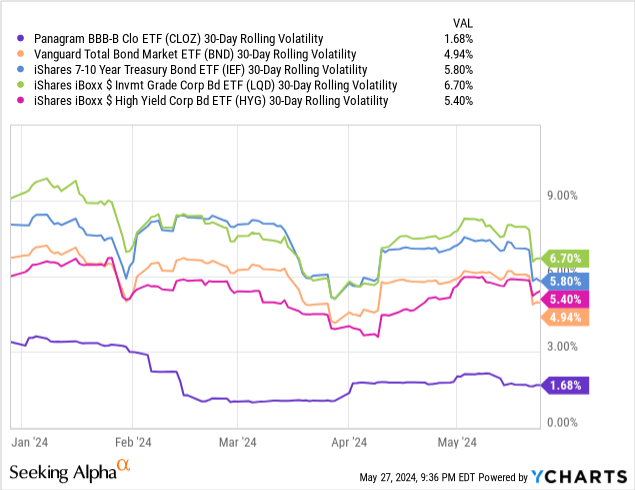

CLOZ has not yet experienced a significant decline or bear market. Realized volatility was very low.

Data by YCharts

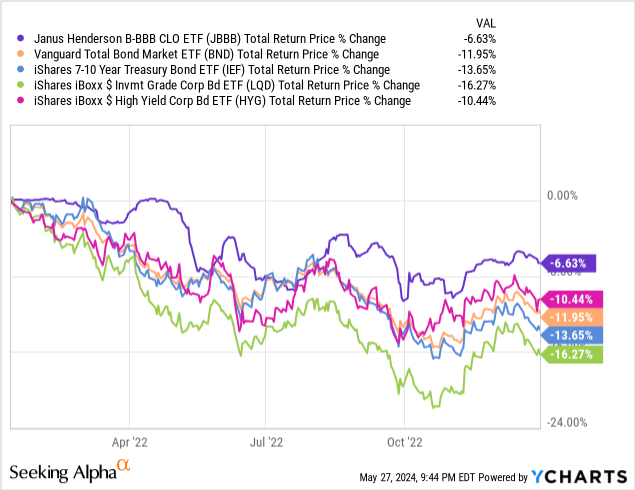

JBBB recorded losses of 6.6% in 2022. The losses were lower than average, but also higher than expected: the fund has no interest rate risk and therefore should not suffer losses when rates are increasing.

Data by YCharts

In any case, CLO debt tranches have overall low credit and interest rate risk, a significant advantage for investors. Excess volatility is certainly a short-term risk and concern, but it is less of a long-term problem.

Performance history

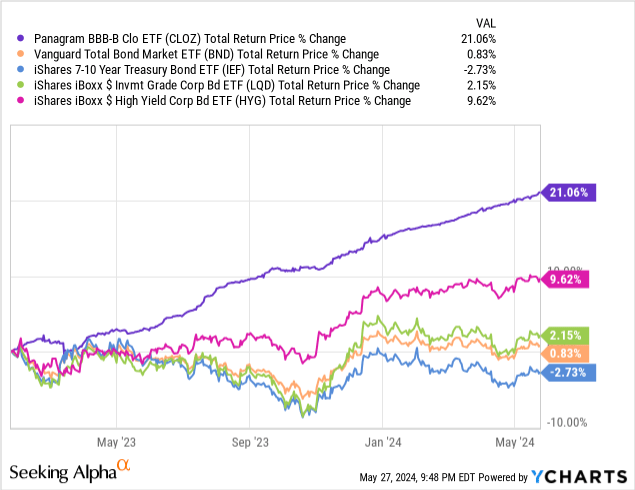

CLOZ has significantly outperformed most bonds and bond sub-asset classes since its inception, partly due to the fund’s strong dividends, partly due to its low interest rate risk.

Data by YCharts

I last covered CLOZ here.

Conclusion

RISR, HYGH and CLOZ are three solid income ETFs and buys. Hopefully the information presented here is useful to readers and provides a useful springboard for those interested in these ETFs.