ETFs

2 High Double-Digit Yield ETFs I’m Buying

James Brey

The context

In the current interest rate environment, it is finally possible to find a significant return. Higher SOFR has driven down valuations, particularly for asset classes with high value and duration, making various income strategies attractive.

Yet even though in nominal terms yields have indeed increased, if we expressed the yield in real terms (i.e. taking into account the rate of inflation), the overall story would no longer seem as attractive.

This means investors must keep looking and, in some cases, move up the risk curve slightly to capture assets that offer tangible returns. Right now, it’s not difficult to find stocks offering dividends of around 5%, but when it comes to yields of 8-10%, the universe of potential choices narrows considerably, especially if we exclude junk bonds and truly speculative instruments.

The potential choice

ETFs based on a covered call strategy are an alternative that offer a return close to or slightly above 10%. The beauty of these products is that they distribute high current income streams fairly consistently, while also introducing some downside protection if the market falls.

The mechanisms underlying how covered call ETFs work are as follows:

- The ETF takes a long position on a certain index (which can also be a very liquid ETF) or replicates its long positions on a particular index such as the S&P 500 or Nasdaq 100.

- Next, a set of call options is sold so that the entire notional asset base is fully exposed to the dynamics of the covered call options.

- The premiums collected on written calls are directly distributed to unitholders.

Returns from collected premiums add an additional layer of defense in the event of a decline in the underlying assets or index.

However, the only major risk of this strategy is related to lost upside potential, since call option writing imposes a cap on the extent to which the underlying assets can appreciate until each incremental increase in price is fully transferred to call option buyers.

For investors following an income-driven portfolio approach, where the most important thing is to achieve above-average returns supported by relatively sustainable instruments, bearing this type of opportunity cost should not be an obstacle.

Two examples

While there are many covered call ETFs out there, the following two are among my favorites.

First of all is the Global X S&P 500 Covered Call ETF (NYSEARCA:XYLD), which is a pure play covered call ETF that sells options using the S&P 500 Index. As with most covered call ETFs, the entire asset base of XYLD is tied to covered call options, implying that the only upside potential from potential price appreciation is limited by the difference between the market price and the strike price of the option at the time an option is written . is sold. A fairly specific aspect of XYLD is the sale of covered calls close to or already at the money. This allows the ETF to produce higher income streams than any average covered call ETF that also bases its strategy on selling call options against the S&P 500. As a result, XYLD is able to offer a yield of 9.4% with very minimal upside potential, making it a decent choice for income-oriented investors for whom the price appreciation component does not have of importance.

Second is the Global X Nasdaq 100 Covered Call ETF (NASDAQ:QYLD), which is a well-known and large ETF that also uses a covered call strategy. The main difference with XYLD is that QYLD writes calls against the Nasdaq-100, while keeping the focus on calls that are at or very close to it. Additionally, when it comes to options frequency, both ETFs stick to a monthly strategy, thereby minimizing the risk of options illiquidity. However, the yield produced by QYLD is approximately 220 basis points higher than that offered by XYLD. The main reason here lies in the only significant difference that exists between these two ETFs, namely QYLD’s exposure to the Nasdaq-100 and not to the S&P 500 as in the case of XYLD. Since the Nasdaq-100 is inherently more volatile due to a combination of a higher concentration in the technology segment and a lower number of underlying components, the affected options are more expensive, resulting in in turn higher yield potential. However, investors need to weigh this against the increased downside risk, which could arise in the event that high-growth and technology names are suddenly penalized or revalued at lower multiples.

The essential

The use of covered call strategies could benefit the portfolio of income-seeking investors, not only by introducing an additional element of diversification, but also by increasing the overall portfolio return. By opting for long covered call ETFs such as XYLD and QYLD, investors can access very juicy returns without taking on unnecessary financial risks. In fact, through these covered call ETFs, investors are exposed to market risk, which is partially reduced by the presence of premiums pocketed when selling covered call options.

Certainly, the downside to covered call ETFs is the opportunity cost associated with any returns from the price appreciation channel, as the options written create a cap on the value appreciation of the options. underlying assets. For XYLD and QYLD, there is limited room for price appreciation given the focus on ATM calls.

However, for investors seeking high income, the advantage of abnormal current income streams with relatively reduced risk may offset the disadvantage of limited price appreciation potential.

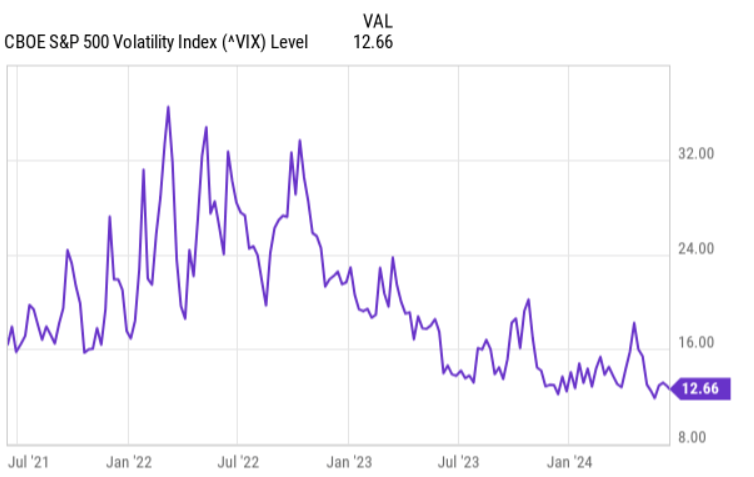

Finally, we all need to consider in this context the fact that the VIX, which measures the implied volatility of the S&P 500 (which also largely reflects the momentum of the Nasdaq-100), is currently trading at rather depressed levels.

Y Charts

Going forward, this implies additional opportunity for covered call ETFs to distribute larger income streams once volatility increases from historic lows.