Fintech

Offline digital payments to address financial exclusion in the non-digital world

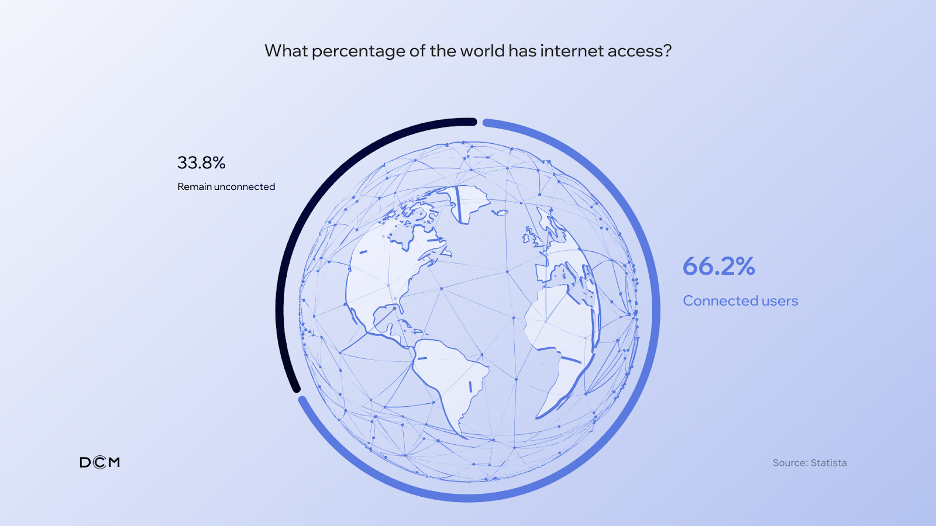

Internet access already seems like something widely accessible and ordinary. Most of our daily activities, including remote work, communication with friends and family, payments, and more, depend on this structure. But is it as accessible as we think? You might be surprised, but just 66.2% of the population globally has access to the Internet. As a result, around 2.65 billion people do not have access to online services and, above all, digital banking and similar services.

The problem may seem distant; however, I am not talking about some emerging economies. Almost six millions of Americans do not have access to banking services. In the meantime, 1.4 billion people outside the United States do not or cannot have a bank account. So, in times when we tap or scan to pay and businesses refuse to accept cash, these people find themselves cut off from the civilized world.

The dependence of digital payments on the internet or telecommunications connectivity is a big problem. Even though we hear a lot of talk about racial wealth gaps and gender-based income inequality, financial exclusion is kept low on the agenda. However, the latter is one of the factors contributing to global poverty, where people cannot access digital financial institutions to save, invest or borrow. They are not welcome in the digital world and are forced to turn to alternative financial organizations, pay high fees, remain buried in this vicious cycle of poverty and use cash. Worldpay’s Global Payments Report 2024 found that the value of cash transactions was $6.1 trillion in 2023, up from $6.7 in 2022. Let’s face it: the 8% year-over-year difference is tiny.

Tapping into offline digital payments, not yet

The development of offline digital payment solutions could significantly address the issue of financial inclusion. However, this is easier said than done. The concept in a nutshell sounds promising, but faces operational, security and technological hurdles. These solutions represent an untapped market with substantial potential, highlighting the need for further research and development to accurately quantify this opportunity.

Furthermore, we should not forget the complexity and costs of existing banking methods. Current transaction fees are still so high that they can easily take up a large percentage of a low-income individual’s small transfer or payment. I hear you say it’s another vicious cycle, but it’s not. The problem is that we are trapped in a narrow mindset regarding the forms and methods of payments.

Playing the winning cards: modern technologies as offline payment tools

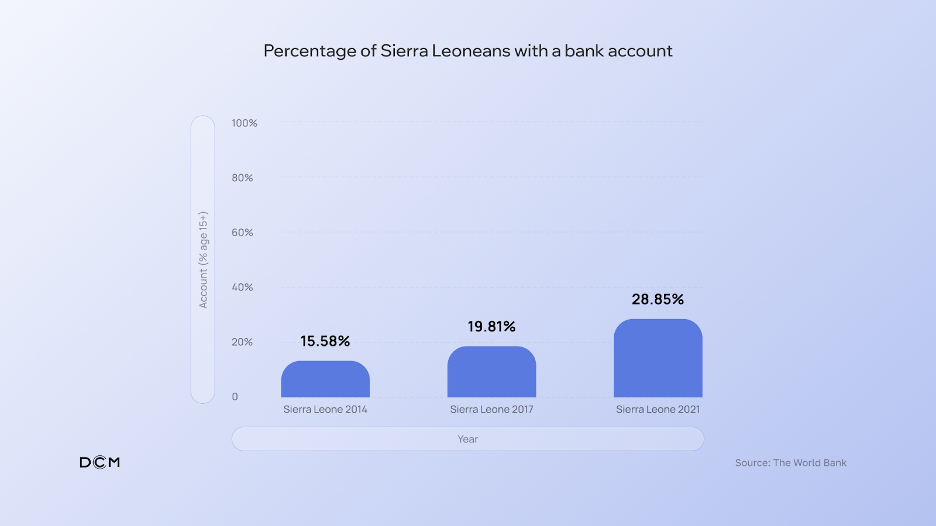

THE case of Sierra Leone’s journey towards financial inclusion highlighted the role of digital financial services in overcoming barriers to banking. In 2014, when the country began receiving technology assistance and grants for digital financial services, only 15.58% of adults had a bank account, despite dozens of commercial/community banks and multiple financial institutions in the country. In 2021, after the first phase of the National Strategy for Financial Inclusion project, these numbers reached 28.85%. In 2023, the government launched the National payment exchange—a financial infrastructure that enables payments interoperability between banks, fintechs and other institutions.

Of course, there is still a lot of work to be done, but the case of Sierra Leone is another proof that modern technologies are the accelerators of inclusive financial services. The use of blockchain technology, central bank digital currencies (CBDCs) and stablecoins could be crucial in the implementation of offline payment infrastructures. These technologies provide a foundation for convenient, secure, and accessible financial services for unbanked populations. How can they make this possible?

Enabling offline transactions for the “not so digital” world.

There are various strategies for offline digital payments, including Near Field Communication (NFC) wallets, QR codes, and token-loaded notes. Each approach presents its own set of challenges and considerations, including device dependency, infrastructure needs, and the need to integrate these technologies into current financial systems. So, let’s take a closer look at each of them.

- Near field communication (NFC) wallets, cards and devices that contain balance data and are able to share it wirelessly with other devices in close proximity. Offline NFC payments are supported by some apps and cards; however, they mostly offer limited functionality or allow transfers within a certain limit. The challenge: the need for a device that activates and supports NFC technology.

- QR Code as a payment operator it represents a more convenient and inclusive way to enable offline payments. In most cases, consumers may face specific limits on the amount or number of offline transactions introduced for security purposes. Additionally, paying via QR code still requires a wallet to store your balance data and an infrastructure to lock the transaction amount. But despite this, it is the best way to process payments offline so far. The challenge: the need for technology to read or process QR codes.

- Notes loaded with tokens—a blockchain offline wallet for storing assets, also known as a Ledger wallet, in the form of a banknote or any other convenient medium that can be loaded with currency to spend offline by managing the banknote to another person offline, like traditional cash. Although it is the most futuristic yet reliable way to enable offline payment using digital money as it can be easily transferred from note-based wallets to digital wallets and vice versa. The challenge: the need for NFC or special minting devices.

The priority task for technology companies is not to give access to traditional banks to those who do not have banking services. In most cases, low-income people do not meet their criteria, such as fees, minimum balances, credit score or others, and therefore remain without banking services. The goal is to provide them with an alternative way to access the benefits of the digital economy. Blockchain technology not only supports the development of digital payment solutions, but also plays a vital role in improving the economic conditions of unbanked populations. Digital banking services, credit and retirement savings could become accessible to even more people around the world, ensuring financial stability and security.

Blockchain-enabled solutions can facilitate secure and efficient transactions, thereby removing barriers to financial inclusion. In this way, companies can promote and support more sustainable and equitable economic development.

-

Ross Kolodiazhnyi is an executive leader and entrepreneur with over 14 years of experience in FinTech, including blockchain, cryptocurrency, RWA tokenization, and artificial intelligence. As CEO of DCM, he builds a cutting-edge SaaS for asset tokenization and financial messaging processing. In his portfolio there are international banks, award-winning regulated and decentralized cryptocurrency and blockchain innovations, and artificial intelligence products.

Lloyds Banking Group and Nationwide have joined an £11m Series A funding round in Scottish artificial intelligence fintech Aveni.

The investment is led by Puma Private Equity with additional participation from Par Equity.

Aveni creates AI products specifically designed to streamline workflows in the financial services industry by analyzing documents and meetings across a range of operational functions, with a focus on financial advisory services and consumer compliance.

The cash injection will help fund the development of a new product, FinLLM, a large-scale language model created specifically for the financial sector in partnership with Lloyds and Nationwide.

Joseph Twigg, CEO of Aveni, explains: “The financial services industry doesn’t need AI models that can quote Shakespeare, it needs AI models that offer transparency, trust and, most importantly, fairness. The way to achieve this is to develop small, highly tuned language models, trained on financial services data, vetted by financial services experts for specific financial services use cases.

“FinLLM’s goal is to set a new standard for the controlled, responsible and ethical adoption of generative AI, outperforming all other generic models in our selected financial services use cases.”

Robin Scher, head of fintech investment at Lloyds Banking Group, says the development programme offers a “massive opportunity” for the financial services industry by streamlining operations and improving customer experience.

“We look forward to supporting Aveni’s growth as we invest in their vision of developing FinLLM together with partners. Our collaboration aims to establish Aveni as a forerunner in AI adoption in the industry, while maintaining a focus on responsible use and customer centricity,” he said.

Treasury Risk Consulting Firm White Matter Alert On Monday he announced the acquisition of a 90% stake in the fintech startup Fair payment for an undisclosed amount. The acquisition will help White Matter Advisory expand its portfolio in the area of cross-border remittance and fundraising services, a statement said. White Matter Advisory, which operates under the name SaveDesk (White Matter Advisory India Pvt Ltd), is engaged in the treasury risk advisory business. It oversees funds under management (FUM) totaling $8 billion, offering advisory services to a wide range of clients.

Improve your technology skills with high-value skills courses

| IIT Delhi | Data Science and Machine Learning Certificate Program | Visit |

| Indian School of Economics | ISB Product Management | Visit |

| MIT xPRO | MIT Technology Leadership and Innovation | Visit |

White Matter Advisory, based in Bangalore, helps companies navigate the complexities of treasury and risk management.

Fairexpay, authorised by the Reserve Bank of India (RBI) under Cohort 2 of the Liberalised Remittance Scheme (LRS) Regulatory Sandbox, boasts features such as best-in-class exchange rates, 24-hour processing times and full security compliance.

“With this acquisition, White Matter Advisory will leverage Fairexpay’s advanced technology platform and regulatory approvals to enhance its services to its clients,” the release reads.

The integration of Fairexpay’s capabilities should provide White Matter Advisory with a competitive advantage in the cross-border remittance and fundraising market, he added.

The release also states that by integrating Fairexpay’s advanced technology, White Matter Advisory aims to offer seamless and convenient cross-border payment solutions, providing customers with secure options for international money transfers.

Rakuten (Japan:4755) has released an update.

Rakuten Group, Inc. and Rakuten Bank, Ltd. announced a delay in the reorganization of Rakuten’s FinTech Business, moving the target date from October 2024 to January 2025. The delay is to allow for a more comprehensive review, taking into account regulatory, shareholder interests and the group’s optimal structure for growth. There are no anticipated changes to Rakuten Bank’s reorganization objectives, structure or listing status outside of the revised timeline.

For more insights on JP:4755 stock, check out TipRanks Stock Analysis Page.

You are reading Entrepreneur India, an international franchise of Entrepreneur Media.

White Matter Advisory, which operates under the name SaveDesk in India, has announced that it is acquiring a 90% stake in fintech startup Fairexpay for an undisclosed amount.

This strategic move aims to strengthen White Matter Advisory’s portfolio in cross-border remittance and fundraising services.

By integrating Fairexpay’s advanced technology, White Matter Advisory aims to offer seamless and convenient cross-border payment solutions, providing customers with secure options for international money transfers.

White Matter Advisory, known for its treasury risk advisory services, manages funds under management (FUM) totaling USD 8 billion.

Founded by Bhaskar Saravana, Saurabh Jain, Kranthi Reddy and Piuesh Daga, White Matter Advisory helps companies effectively manage the complexities of treasury and risk management.

The SaveDesk platform offering includes a SaaS-based FX market data platform with real-time feeds for over 100 currencies, bank cost optimization services, customized treasury risk management solutions, and compliance guidance for the Foreign Exchange Management Act (FEMA) and other trade regulations.

Fairexpay is a global aggregation platform offering competitive currency exchange rates from numerous exchange partners worldwide. Catering to both private and corporate customers, Fairexpay provides seamless money transfer solutions for education, travel and immigration, as well as simplifying cross-border payments via API and white-label solutions for businesses. Key features include competitive currency exchange rates, 24-hour processing times, extensive currency coverage of over 30 currencies in more than 200 countries, and secure, RBI-compliant transactions.

“This could be the greatest coverage in history” – Whitney leaves a new bomb

Start! This market model is about to unleash the biggest manifestation ever – Dylan Leclair

“The list of epstein is real and Trump knows who he is on it” – Whitney Webb makes New Epstein Bombshell fall

“I did mathematics! Bitcoin is about to destroy records” – Samson Mow and Jack Mallers

“Blackrock games exposed: you are watching a bull that are engineered” – Matt Hugan

Switchboard Revolutionizes DeFi with New Oracle Aggregator

Latest Business News Live Updates Today, July 11, 2024

Is Zypto Wallet a Reliable Choice for DeFi Users?

👀 Lido prepares its response to the recovery boom

FinTech LIVE New York: Mastercard and the Power of Partnership

“This could be the greatest coverage in history” – Whitney leaves a new bomb

Start! This market model is about to unleash the biggest manifestation ever – Dylan Leclair

“The list of epstein is real and Trump knows who he is on it” – Whitney Webb makes New Epstein Bombshell fall

“I did mathematics! Bitcoin is about to destroy records” – Samson Mow and Jack Mallers

“Blackrock games exposed: you are watching a bull that are engineered” – Matt Hugan

-

DeFi1 year ago

DeFi1 year agoSwitchboard Revolutionizes DeFi with New Oracle Aggregator

-

News1 year ago

News1 year agoLatest Business News Live Updates Today, July 11, 2024

-

DeFi1 year ago

DeFi1 year agoIs Zypto Wallet a Reliable Choice for DeFi Users?

-

DeFi1 year ago

DeFi1 year ago👀 Lido prepares its response to the recovery boom

-

Fintech1 year ago

Fintech1 year agoFinTech LIVE New York: Mastercard and the Power of Partnership

-

DeFi1 year ago

DeFi1 year agoEthena downplays danger of letting traders use USDe to back risky bets – DL News

-

Fintech1 year ago

Fintech1 year ago121 Top Fintech Companies & Startups To Know In 2024

-

ETFs1 year ago

ETFs1 year agoGold ETFs see first outing after March 2023 at ₹396 cr on profit booking

-

Fintech1 year ago

Fintech1 year agoFintech unicorn Zeta launches credit as a UPI-linked service for banks

-

DeFi1 year ago

DeFi1 year agoTON Network Surpasses $200M TVL, Boosted by Open League and DeFi Growth ⋆ ZyCrypto

-

ETFs1 year ago

ETFs1 year agoLargest US Bank Invests in Spot BTC ETFs While Dimon Remains a Bitcoin Hater ⋆ ZyCrypto

-

News1 year ago

News1 year agoSalesforce Q1 2025 Earnings Report (CRM)