Fintech

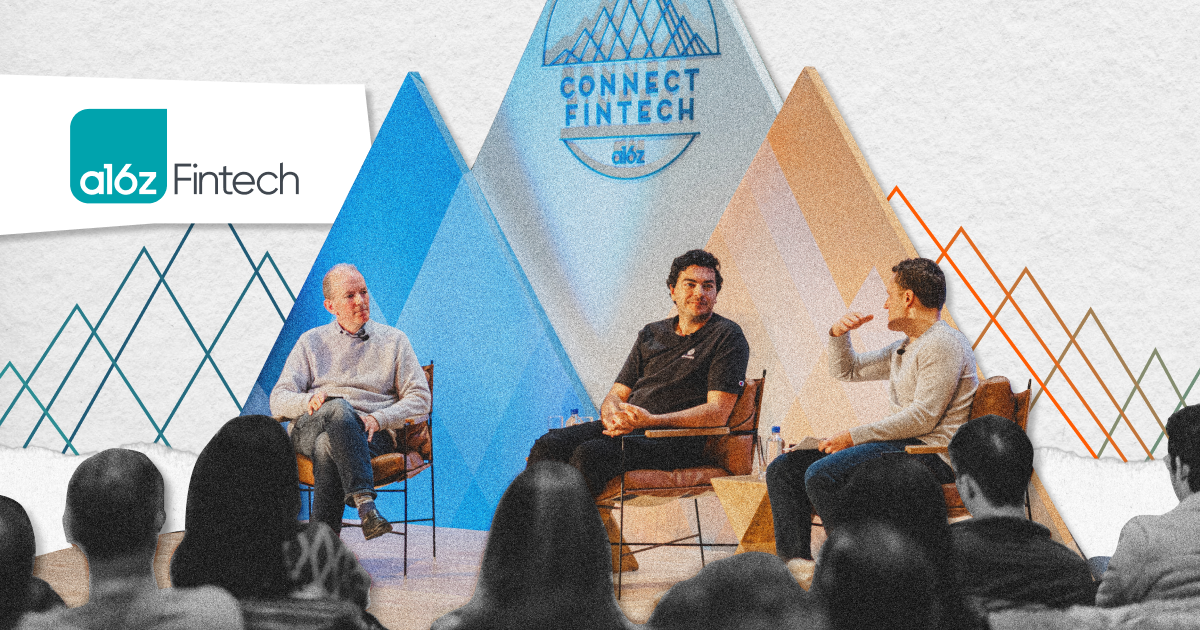

Forecasting Fintech’s Future and Keeping Culture Alive: A Q&A with the CEOs of BILL and Mercury

At a16z’s recent Connect/Fintech event, a16z Partner Alex Immerman sat down for a broad conversation with Immad Akhund, co-founder and CEO of Mercury, and René Lacerte, founder and CEO of financial services company BILL.

They discussed the wide-ranging implications that generative AI will have across fintech and how it will boost jobs, rather than replace them. They also talked about the difficulties — and potential advantages — of selling into small businesses, taking alternative approaches to interviewing candidates, and the importance of keeping culture a vital part of a company as it scales.

Here’s an edited excerpt from their conversation.

Alex Immerman: If 2023 was the year of efficiency, 2024 is the year of generative AI. I know the two of you have been using “old school” AI for some time now, but why don’t we start with how you’re using GenAI in your companies?

René Lacerte: Trust around money is one of the most important things that society has, and how we make sure we’re enhancing trust is something I think about a lot. When I think about AI, the most important thing is how do we leverage the data that we have to actually create that trust environment for our customers.

We have a ton of AI around money movement we do around payables, money movement we do around credit and extending credit, and accelerating and approving loans automatically, etc. It’s still not GenAI.

GenAI comes in to make employees efficient. Whether it’s creating better tools to write code and test code, better tools for customers to engage with reps, better tools for sales teams to engage with their prospects, all those things are happening inside of Bill. We have to create our own GenAI for the customer. And that takes time, and is not something we’re going to do willy-nilly.

Immad Akhund: We’ve done a couple of things that are customer facing. For our help desk, GenAI is really good for that. Also, scanning the receipt, GenAI actually beats optical character recognition (OCR) that’s specifically made for receipt scanning, which I thought was kind of interesting. So we tried these ways internally in the company. We haven’t, at least so far, seen massive efficiency gains.

My general view is that every part of AI will be way better next year. So unless there’s some really obvious or transformative thing to do in your business today, it’s worth waiting a little bit to invest heavily in that. We’re experimenting with it, but we haven’t made a massive investment.

René: You can’t have hallucinations when it comes to fintech, the risk is super high. I think we have to explore in pockets, like we use GenAI around receipt scanning, but we also have our own AI around receipt digesting. I think it will continue to get better, and that’s going to make a big difference over time.

Alex: What do you think are the key breakthroughs? Are there regulatory obstacles to overcome that would enable you to adopt more GenAI?

René: The core cornerstone of everything that’s happening with AI is you have to have the right data to be able to create the models. The first thing I would ask is, “where are you pulling the data?” Public data is not the same as the data that we have transactionally, it’s not the same as any of the companies here have. Rocket Mortgage has 30 years of data around mortgages in different markets. They can build a much better model around predicting than anybody else could on the outside. That data is not public. My answer is: you’ve got to have the right data.

Alex: Let’s forecast out. It’s 2034. How do you think the role of a financial controller or CFO is going to evolve over the next 10 years?

René: If you go back to what accountants were 60 years ago, before I was born, before technology came in, accountants actually were the trusted partner that was adding advice, because they did everything. And that’s what I think is coming full circle. Technology is going to enable people to get out of the mundane tasks of running their business, and accountants, or people like accountants, CFOs, whatnot, will be strategic advisors.

You won’t be worried about how the wire got made, you’ll be able to say, “that supplier is really good, let’s pay them more, let’s do more with them.” All those things are the conversations you need to have, and we already see that happening.

I don’t believe jobs go away. I believe people specialize and become experts. And I think they’ll use the tools to become experts.

Alex: Immad has strong feelings about AI replacing engineers. Mind sharing?

Immad: As an engineer, I’m obviously a little biased. You can make a prototype with AI, but are you going to be able to take that million-line codebase and figure out what to do? I do think engineers will be significantly enhanced. Maybe every engineer is a 10x engineer and the 10x has become 20x, or something. But I think we would need artificial general intelligence (AGI)-level AI before an engineer is fully replaced.

Alex: Let’s dive into your business models. Both of you sell into SMBs, which is a notoriously difficult segment. One of the holy grails of SMB software is, how are you going to acquire customers? You’ve both done a pretty darn good job at it. Rene, start with the early days and how you acquired your first customers.

René: I grew up in a family of entrepreneurs, half a dozen businesses, each for parents and grandparents, and all of them serving small businesses since the ‘60s. So I grew up serving SMBs and being in love with what they do for society.

I knew they’re too busy to have to trust somebody new. But they do trust their accountants, and they do trust their banks. So our distribution channel has always been to go direct, and we get great customers direct. But then go through third parties, accountants, and partners. And the first partnerships were banks, and now we have other partnerships.

The opportunity is to leverage that trust factor to drive customer acquisition, and it has worked for us. It’s an opportunity for us to continue to leverage that ecosystem that we’ve built.

Immad: I find it funny that everyone complains about the difficulty of SMB and consumer customer acquisition, but ironically, SMB and consumer companies are some of the most valuable. And I think that’s because it is harder to get distribution. But if you can do it, it’s more valuable.

I’ve been an entrepreneur since 2006. When you’re starting a new company, you ask “who should I use for banking, who should I use for card processing, payroll, etc.?” That was a realization I had, that no one was happy with the default choice. When we started, it was mostly SVB. But it’s still a very core part of Mercury to get entrepreneurs to tell each other about us.

Alex: The other side of the equation on customer acquisition is monetization. One of the criticisms of SMB software is that each customer can only provide so much revenue. For both of you, subscription is a smaller-to-no piece of the story. BILL started much heavier on subscription, but has really leaned into payments over the last several years. Mercury has never monetized via subscription and just focused on payments and float. What do you think the role of subscriptions are in B2B fintech? Or do you think great software just earns the right to monetize on payments and float?

René: Even though subscription is less than 30% of our overall revenue, it’s still the cornerstone. The customer comes to us because they need software to manage their financial operations. If we do a great job of giving them software, guess what, they’ll take the payment products we have.

From the time we went public, a little over 4 years ago, the trailing revenue was $100 million. Now we’re over a billion dollars. So to 10x in 4 years, some of it was software, but some was just adding all the capabilities that we added with payments and having a great integration with payments, whether it was international, or card, or instant transfer. I wouldn’t look at the subscription revenue percentage as whether it’s a sufficient business or not, we are definitely a subscription business. Every transaction comes from a subscribing customer on the bill side, on the spending expense. It’s a transaction business. The software’s given way to bring people in so they have the card spend experience that they don’t have any place else.

Immad: Yeah, I’ve been doing startups a long time, and like fintech is great. It scales with your customers. If we have a tiny SMB doing almost nothing on Mercury, we’re not charging them anything, basically. Whereas we have bigger companies that we end up making money on. I think it’s a good business model.

Alex: There are plenty of great businesses that don’t have subscription models. But many companies, particularly in your adjacent spaces that have only monetized for most of their history via interchange or transactional revenue, are now leaning more into subscription.

René: Being public, I think the question that I hear from investors, at least indirectly, is how sticky is the revenue? I do think it’s important.

Alex: A lot of fintech founders wrestle with the question: should we hire for the “fin” or for the “tech?” Should we hire from financial services, or should we hire from software backgrounds? How have you thought about that?

René: It probably depends on the situation. What’s the actual experience that you’re trying to work on? If it was purely a payments business, then I might focus on payments. I would probably lean more heavily for us on, “Do you know how to build great software that customers are going to love?” And we haven’t talked about regulatory, but making sure you have that covered. That’s super, super important.

Immad: We much, much prefer getting someone from another fintech. Ideally, if they had banking experience and then they went to a fintech. Luckily for us, many fintechs have been around long enough so there’s plenty of talent to get.

Alex: You are two of the sharpest talent thinkers I know. What are your strategies for recruiting and retaining talent within your respective organizations?

Immad: We care a lot about culture, and we have that well defined. We’re looking for humble, helpful, low-ego people, very active first-principle thinkers. Then we try to take those cultural attributes and turn them into actual, consistent hiring interviews that we do across a bunch of roles. For example, we have a product interview where we ask them a hypothetical question. The most recent one is: how would you improve the Uber experience?

Of course, we learn what’s a good answer, how to ask questions, etc. We also have a casual interview that we call the presentation interview. We give people an hour to write a presentation on any topic of their choice.

Alex: Does it have to be related to Mercury?

Immad: It doesn’t have to. We’ve had someone talking about how to look after chickens in a chicken coop.

Alex: Did they get hired?

Immad: Yeah, she’s amazing. But you can go very deep on every subject with these kinds of interviews, I think those are fun for us, as well.

Silicon Valley has this mentality of people staying at a company for two years and then leaving. I don’t know how you build a company like that. We’ve done a ton of things to encourage and look for people who are in it for a slightly longer term.

René: I don’t use job descriptions, I use job scorecards. A scorecard is where you look out into the future 3 months, 6 months, 9 months, 18 months out, and this is what you will have accomplished.

Some people are like, how would I do that? And they don’t even apply. Other people ask “why is it that low?” And then that’s a good conversation, and that kind of becomes their onboarding.

Additionally, which everybody already knows, but it’s hard to put in practice, you’ve got to fire quickly. Nobody wants to go there. No VC, no employer, nobody wants to think about firing, but if it enters your mind, you probably should do it.

I would say, part of hiring is also firing. If you want good retention, you’ve got to actually fire the low performers, because that creates a high bar and high performance culture and the 10xers, that’s what they like seeing.

Alex: We’re going to wrap up with a lightning round. Biggest threat to your business in 5 to 10 years?

Immad: Our culture degrading.

René: The unknown competitor. Whether it’s AI driven or not.

Alex: If you’re starting your company today, would you be fully remote, hybrid, or fully in the office?

René: In the office. You’ve got to build camaraderie. So people finish each other’s sentences and they think about each other when they’re not with each other. And Zoom doesn’t do as good a job.

Immad: Pre-product market fit, we’d definitely be in an office.

Alex: Regulation: a headwind or a tailwind for you?

René: I think it is actually healthy. I’m probably one of the rare guys who actually says regulation is good. We are better when our 50 state regulators come in and they tell us something. It ends up helping all of our customers. I would say it ends up being a tailwind because we embrace it. But there’s work.

Immad: I would say short term headwind, medium-long term tailwind.

Alex: What fintech company do you admire most that’s not sitting next to you?

René: Square, because they did hardware, software, and payments all at once. To do all those things at once is pretty powerful.

Immad: I guess I have to take Stripe then. They’ve always set a very high quality bar, and I appreciate that.

Alex: Thank you both for sharing your thoughts here.

Lloyds Banking Group and Nationwide have joined an £11m Series A funding round in Scottish artificial intelligence fintech Aveni.

The investment is led by Puma Private Equity with additional participation from Par Equity.

Aveni creates AI products specifically designed to streamline workflows in the financial services industry by analyzing documents and meetings across a range of operational functions, with a focus on financial advisory services and consumer compliance.

The cash injection will help fund the development of a new product, FinLLM, a large-scale language model created specifically for the financial sector in partnership with Lloyds and Nationwide.

Joseph Twigg, CEO of Aveni, explains: “The financial services industry doesn’t need AI models that can quote Shakespeare, it needs AI models that offer transparency, trust and, most importantly, fairness. The way to achieve this is to develop small, highly tuned language models, trained on financial services data, vetted by financial services experts for specific financial services use cases.

“FinLLM’s goal is to set a new standard for the controlled, responsible and ethical adoption of generative AI, outperforming all other generic models in our selected financial services use cases.”

Robin Scher, head of fintech investment at Lloyds Banking Group, says the development programme offers a “massive opportunity” for the financial services industry by streamlining operations and improving customer experience.

“We look forward to supporting Aveni’s growth as we invest in their vision of developing FinLLM together with partners. Our collaboration aims to establish Aveni as a forerunner in AI adoption in the industry, while maintaining a focus on responsible use and customer centricity,” he said.

Treasury Risk Consulting Firm White Matter Alert On Monday he announced the acquisition of a 90% stake in the fintech startup Fair payment for an undisclosed amount. The acquisition will help White Matter Advisory expand its portfolio in the area of cross-border remittance and fundraising services, a statement said. White Matter Advisory, which operates under the name SaveDesk (White Matter Advisory India Pvt Ltd), is engaged in the treasury risk advisory business. It oversees funds under management (FUM) totaling $8 billion, offering advisory services to a wide range of clients.

Improve your technology skills with high-value skills courses

| IIT Delhi | Data Science and Machine Learning Certificate Program | Visit |

| Indian School of Economics | ISB Product Management | Visit |

| MIT xPRO | MIT Technology Leadership and Innovation | Visit |

White Matter Advisory, based in Bangalore, helps companies navigate the complexities of treasury and risk management.

Fairexpay, authorised by the Reserve Bank of India (RBI) under Cohort 2 of the Liberalised Remittance Scheme (LRS) Regulatory Sandbox, boasts features such as best-in-class exchange rates, 24-hour processing times and full security compliance.

“With this acquisition, White Matter Advisory will leverage Fairexpay’s advanced technology platform and regulatory approvals to enhance its services to its clients,” the release reads.

The integration of Fairexpay’s capabilities should provide White Matter Advisory with a competitive advantage in the cross-border remittance and fundraising market, he added.

The release also states that by integrating Fairexpay’s advanced technology, White Matter Advisory aims to offer seamless and convenient cross-border payment solutions, providing customers with secure options for international money transfers.

Rakuten (Japan:4755) has released an update.

Rakuten Group, Inc. and Rakuten Bank, Ltd. announced a delay in the reorganization of Rakuten’s FinTech Business, moving the target date from October 2024 to January 2025. The delay is to allow for a more comprehensive review, taking into account regulatory, shareholder interests and the group’s optimal structure for growth. There are no anticipated changes to Rakuten Bank’s reorganization objectives, structure or listing status outside of the revised timeline.

For more insights on JP:4755 stock, check out TipRanks Stock Analysis Page.

You are reading Entrepreneur India, an international franchise of Entrepreneur Media.

White Matter Advisory, which operates under the name SaveDesk in India, has announced that it is acquiring a 90% stake in fintech startup Fairexpay for an undisclosed amount.

This strategic move aims to strengthen White Matter Advisory’s portfolio in cross-border remittance and fundraising services.

By integrating Fairexpay’s advanced technology, White Matter Advisory aims to offer seamless and convenient cross-border payment solutions, providing customers with secure options for international money transfers.

White Matter Advisory, known for its treasury risk advisory services, manages funds under management (FUM) totaling USD 8 billion.

Founded by Bhaskar Saravana, Saurabh Jain, Kranthi Reddy and Piuesh Daga, White Matter Advisory helps companies effectively manage the complexities of treasury and risk management.

The SaveDesk platform offering includes a SaaS-based FX market data platform with real-time feeds for over 100 currencies, bank cost optimization services, customized treasury risk management solutions, and compliance guidance for the Foreign Exchange Management Act (FEMA) and other trade regulations.

Fairexpay is a global aggregation platform offering competitive currency exchange rates from numerous exchange partners worldwide. Catering to both private and corporate customers, Fairexpay provides seamless money transfer solutions for education, travel and immigration, as well as simplifying cross-border payments via API and white-label solutions for businesses. Key features include competitive currency exchange rates, 24-hour processing times, extensive currency coverage of over 30 currencies in more than 200 countries, and secure, RBI-compliant transactions.

“Prepare for a massive explosion top for Crypto in 2025” – Matt Hugan and Dan Tapiero

Michael Saylor – “The real Bitcoin Bull Run is about to start shortly”

“Bitcoin’s opportunity from $ 700x nobody sees arriving in 2025” – Willy Woo & Raoul Pal

‘The next Bitcoin holder bond at this crucial level ” – Tom Lee

Jeff Booth – We made a 100% wrong on the bull market

Switchboard Revolutionizes DeFi with New Oracle Aggregator

Latest Business News Live Updates Today, July 11, 2024

Is Zypto Wallet a Reliable Choice for DeFi Users?

👀 Lido prepares its response to the recovery boom

FinTech LIVE New York: Mastercard and the Power of Partnership

“Prepare for a massive explosion top for Crypto in 2025” – Matt Hugan and Dan Tapiero

Michael Saylor – “The real Bitcoin Bull Run is about to start shortly”

“Bitcoin’s opportunity from $ 700x nobody sees arriving in 2025” – Willy Woo & Raoul Pal

‘The next Bitcoin holder bond at this crucial level ” – Tom Lee

Jeff Booth – We made a 100% wrong on the bull market

-

DeFi11 months ago

DeFi11 months agoSwitchboard Revolutionizes DeFi with New Oracle Aggregator

-

News11 months ago

News11 months agoLatest Business News Live Updates Today, July 11, 2024

-

DeFi11 months ago

DeFi11 months agoIs Zypto Wallet a Reliable Choice for DeFi Users?

-

DeFi1 year ago

DeFi1 year ago👀 Lido prepares its response to the recovery boom

-

Fintech11 months ago

Fintech11 months agoFinTech LIVE New York: Mastercard and the Power of Partnership

-

DeFi11 months ago

DeFi11 months agoEthena downplays danger of letting traders use USDe to back risky bets – DL News

-

Fintech1 year ago

Fintech1 year ago121 Top Fintech Companies & Startups To Know In 2024

-

Fintech1 year ago

Fintech1 year agoFintech unicorn Zeta launches credit as a UPI-linked service for banks

-

News1 year ago

News1 year agoSalesforce Q1 2025 Earnings Report (CRM)

-

ETFs1 year ago

ETFs1 year agoGold ETFs see first outing after March 2023 at ₹396 cr on profit booking

-

Videos1 year ago

Videos1 year ago“We will enter the ‘banana zone’ in 2 WEEKS! Cryptocurrency prices will quadruple!” – Raoul Pal

-

Videos1 year ago

Videos1 year ago“BlackRock HAS UNLEASHED a massive multi-trillion monster” – Lyn Alden and Eric Balchunas